A Must See! 30 Minutes of Vital, Never-Before-Heard Information.

Lynette Zang is the chief market analyst at ITM Trading. For quite some time now she has been producing YouTube Videos which convert complex market information into usable information that is easy for everyone to understand. Lynette has a way of taking the complex and presenting it in a simple fashion. Additionally, she has the dogged determination to chase down and present the facts to accompany and support her presentation. ITM Trading suggests that you begin watching Lynette’s YouTube series by viewing her Video entitled 2008 Was Just A Warning. This article (which will chronicle Lynette’s Presentation) will show you that the crash of 2008 was a warning, and that you absolutely must prepare for the (inevitable) next event. This next crash may also be so unsolvable, that it leads to a complete financial reset.

When you see some of the numbers and facts Lynette presents in her Video, perhaps you will agree that the upcoming crash will make the 2008 recession seem very mild in comparison. The problems that caused 2008 were never fixed, they were merely papered over…

It should be said Lynette has a background as a stockbroker and as a banker, and that she has been participating in these markets since the 1960s. Lynette likes to say that she was groomed for financial times and situations just like these. After watching this very informative and interesting video (and/or reading this article) you may just agree.

The Crash Of 2008 Was A Warning : Currency Life-cycles.

When Lynette worked as a stockbroker she worked primarily with non-dollar-denominated bonds. This is what led her to study currencies. She learned the currencies have a visible and consistent life-cycle. By watching for a few things you can see which stage of the life-cycle the currency is in. Lynette contends that by being able to recognize the stages and trends of the currency life-cycle there is a much better chance that you can be in the right place at the right time with the right asset and prosper during challenging times.

Lynette used her knowledge of currencies to develop a strategy for herself. Today she would like to share part of that strategy with you. This is why Lynette feels that it is important that you take the time to understand the strategy: there is a currency war going on. A currency war puts all of your wealth and future plans in jeopardy. A currency war erodes the very foundation of the global financial system is based on; money.

A Reminder About 2008.

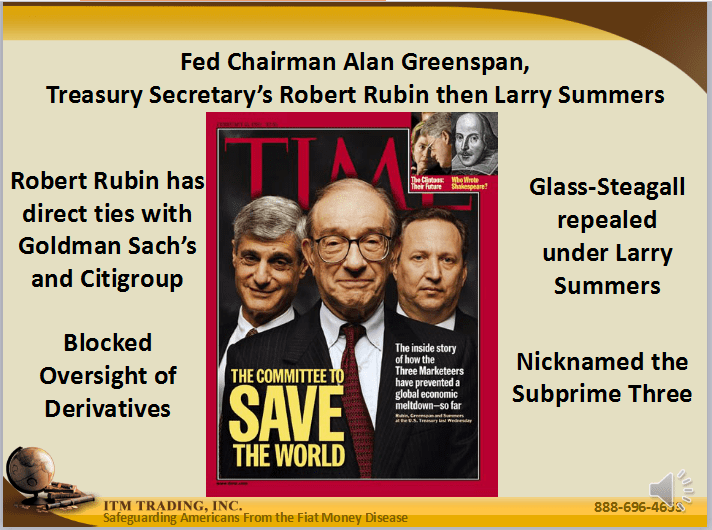

In 2008 a mortgage derivative debt bubble burst. This sent the world into what was known as the Great Recession. AIG was given taxpayer bailout money to make good at 100 cents on the dollar worthless derivative bets that they had made with Goldman Sachs and JP Morgan Chase and other large banks. Trillions of dollars of wealth evaporated and credit dried up overnight.

Lynette reminds us that Bear Stearns was sold for pennies on the dollar and that Merrill Lynch was saved from bankruptcy by Bank of America. The Federal Reserve allowed Lehman Brothers to fail. Stock markets imploded and emergency actions had to be taken. Interest rates were lowered to near zero.

Trillions of dollars were injected into the financial system in emergency actions. All of the central banks around the world were at the ready to begin printing huge sums of money. And, ever since 2008 the central banks have been printing huge sums of money.

In the following parts of the webinar, Lynette will take you deep into the inner workings of the global financial system. Lynette listens to what the central bankers say. However, Lynette also watches what they do.

The Key Players.

The Federal Reserve is a private central bank which Lynette notes was put in charge of our money In 1913. The Federal Reserve was formed by contract charter. The Federal Reserve was further legalized by the Federal Reserve act. Because the US dollar is the most used currency in international trade, the actions of the Federal Reserve have a strong global impact.

2008 Was A Warning.

Lynette states that if you combine the Federal Reserve with all of the other central banks, as well as the Bank for International Settlements (BIS), which is the central banker’s central bank, you have the most powerful and influential group of bankers in the world. She believes that the intent and design of these central bankers is to organize a financial system reset.

A reset is one way a government declares bankruptcy. Governments devalue their currency to pay the debts that they cannot afford. Eventually, this creates hyperinflation. In the future, Lynette believes the United States dollar will experience hyperinflation.

Hyperinflation, however, will create opportunities. Gold is an asset that holds your purchasing power during hyperinflation. In the webinar, Lynette will review a few key concepts such as good money, fiat money, and the fiat money disease. Lynette maintains that the crash of 2008 was a warning. The threats that we face today are much greater. Lynette will show you that new ownership laws jeopardize your wealth, but that there is an opportunity to be captured.

The Crash Of 2008 Was A Warning : Money.

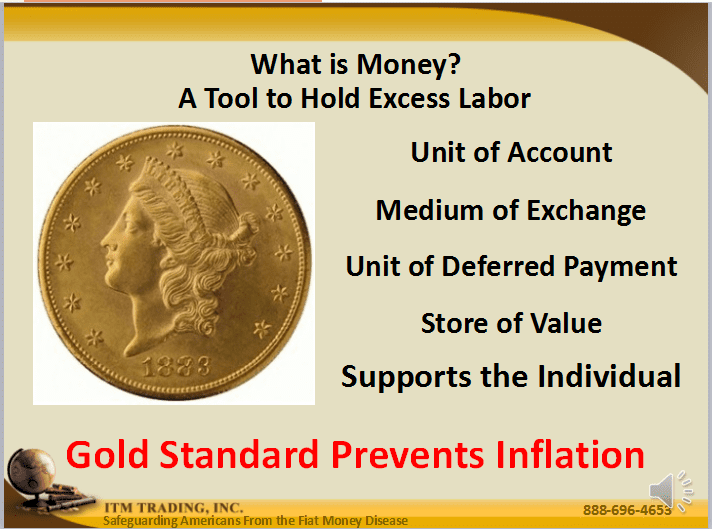

What is money? Originally, money was developed to store excess labor. Money also allowed labor specialization. In order to function, money needs to be indestructible, easy to carry and divisible. Money should also hold value over time. It takes labor to mine gold and silver. Therefore, this makes gold and silver easy to value since labor equals labor. This created a standard against which all goods and services could be fairly valued.

2008 Was A Warning.

Over thousands of years, many forms of money have been tried. However, only gold and silver have met all of the criteria above. This is why gold and silver have been known as good money for the last 6000 years.

Lynette goes on to explain that the four pillars of money are: a unit of account, a unit of exchange, a unit of deferred payment and a store of value. Purchasing power integrity allows you to purchase the same goods and services at a later time for the same price you could purchase them today. This is the most important function of money performs.

2008 Was A Warning.

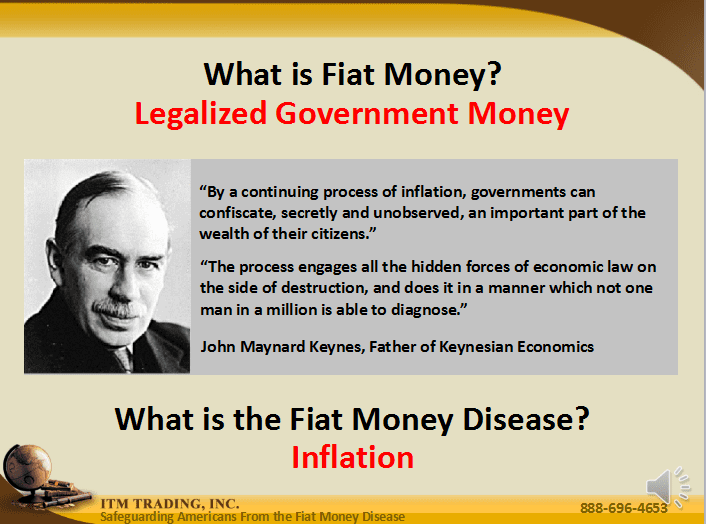

When gold and silver coins were used as money the people owned them held their wealth outright. Wealth was held outside of the banking system. However, the gold standard is constraining for governments and central banks. So, a new system was created called “fiat”. In a fiat system, money is borrowed into existence. Fiat money mimics good money, but the most important function of fiat money is inflation. Inflation guarantees that you cannot by the same amount of goods the same amount of money in the future.

2008 Was A Warning

The Gold Standard And Pegs.

Prior to 1913, the United States was on the gold standard. 1/20 of an ounce of gold was pegged to every one US dollar. After 1913 the peg was shifted to where 1/20 an ounce of gold was worth $2.40. Lynette shares that by 1928 the pegs and the markets were both breaking down. The Great Depression happened and all confidence in the fiat money system was lost.

In 1933 laws were changed and the government and central bank were the only ones allowed to hold monetary gold. Once those laws were in place, a new gold peg was created. This time 1/20 of an ounce of gold backed four dollars. In 1971 the final gold peg was broken when Pres. Nixon removed the United States from the last vestiges of the gold standard. The pure fiat dollar was born. Today the US dollar is not backed by anything other than debt and confidence.

Over time, since all international currencies eventually became fiat, currencies started pegging to each other to establish value. In January 2015, those pegs began breaking. The Swiss franc violently de-pegged from the euro dollar. Lynette states that the most visible peg shift occurred between the US dollar and the Chinese yuan. On August 11th, 2015, when this happened, the global markets began to deflate.

Inflation.

There is only one way to fight deflation, and that is with inflation. And, Lynette says that inflation is the only tool that central bankers have left. What history tells us is the most likely outcome of massive money printing is hyperinflation. When all confidence in the currency is lost, the cycle comes full circle and currencies are supported by gold again in order to restore confidence.

The peg is related to how much fiat money can be created. The backing, however, relates more to purchasing power. Lynette points out that you might recognize this lack of purchasing power as inflation. The bankers do this by design, and if you listen to them closely they are telling us that they are not done inflating the dollar. Next, Lynette points out that inflation is the fiat money disease. Good money, however, cannot be inflated away.

The 2008 crisis made the fiat money disease possible. Until the central bankers had the ability to print money without limits, the ability to prop up the imploding markets would never have existed. And, Lynette points out that the problems that caused 2008 were never fixed.

Why The Crash Of 2008 Was A Warning.Â

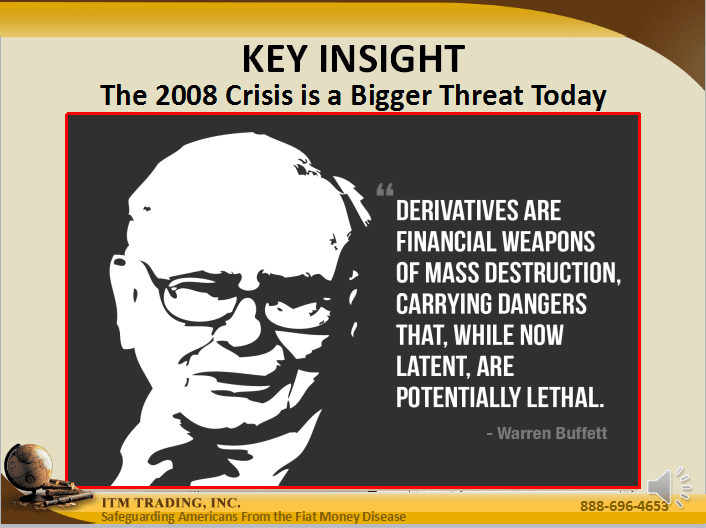

The entire fiat money system is intangible. Bankers create complex contracts for banks. They support these by ever-expanding levels of credit and debt. Derivatives, Lynette says, are the most dangerous of these contracts. Derivatives can only be converted into fiat. And, most derivatives are created off the balance sheet which means that these liabilities are out of sight of the investor.

Lynette reminds us that it was a mortgage derivative explosion that triggered the 2008 crisis. She then points out that many central bankers say the financial issues are not resolved. Rather, the issues of only grown larger. The markets are less liquid and more fragile. Everyone is much more vulnerable.

In 2008, some of the largest and most respected firms either went bankrupt or were absorbed by banks that were given taxpayer bailouts. The taxpayers and depositors are now the ones who are responsible for the financial problems of the banks.

The Crash Of 2008 Was A Warning : Derivatives.

Warren Buffett has called derivatives weapons of mass financial destruction. In addition to usual market risk, derivatives create additional unseen market risk. These risks threaten the abilities of the central bankers to support the financial system during the next liquidity crisis.

2008 Was A Warning.

The purpose of the Dodd-Frank act was to move investment products out of depository banks. But, the big banks lobbied and kept investment products within the FDIC system. This threatens bank deposits. The bail-in provisions within Dodd-Frank require that all assets of the bank be used before tax-payer bail-out provisions are used. This makes all deposits vulnerable to a derivative default.

In addition, these derivatives are sold into mutual funds and other investment vehicles and this adds a lot of risk to the unsuspecting public. This may threaten your investment and retirement accounts. These are just some of the many reasons derivatives matter to you.

The Size Of The Problem.

In an attempt to put into perspective the size of the problem, Lynette offers this example.

“1 million seconds ago was 12 days. 1 billion seconds ago was 1983. 1 trillion seconds ago was 29,704 BC.”

More perspective:

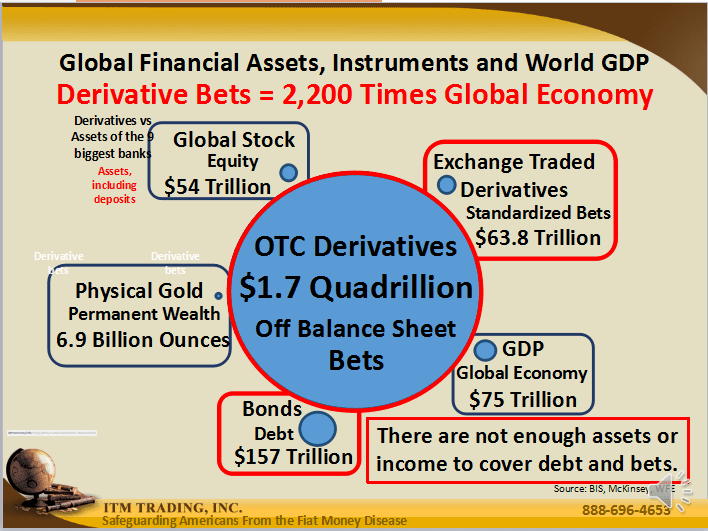

The amount of money that moves through the global economy is $75 trillion. (Global GDP)

The derivatives game is much like a closed poker game. Only those that are too big to fail can play. No one needs to bring money to the game, everything is done with credit. There are really no rules and no limits. And since the FDIC backstops all of the bets, bank risk is limited.

Once the game begins the banks start betting between themselves until everybody has bets with everybody else. Every time a new bet is placed someone makes money and as long as the fees are paid, the bets never have to be settled. However, there are also no limitations on losses.

How Big Is the Threat?

2008 Was A Warning.

The fiat money system is infinite thanks to technology. Lynette says that prior to a change in accounting procedures the Bank of International Settlements stated that there was 1.7 quadrillion dollars worth of over-the-counter derivatives in existence.

This means that the derivative market that we cannot track and that we cannot see is over 2200 times the size of all the fiat money that flows through the entire global economy. The Comptroller of the office of the currency says that roughly 79% of all derivatives are interest rate related and a rapid spike in interest rates could trigger an explosion that would make 2008 look tame in comparison. The mortgage derivative bets that triggered 2008 were tiny in comparison to today’s interest rate derivative bets.

Why Your Deposits Are at Risk.

Over 91% of the reported derivatives are held by the top four banks. All of these banks are deemed too big to fail. The average derivative bet in those banks is 114 times as much as their assets. Lynette reminds us here that their assets include your deposits. Almost all of those bets are off the bank balance sheet. This means investors don’t know about the instability and debt. A derivative explosion in any one of these banks can easily topple the global financial system. This will take your deposits and every other financial product that you own. The US banking system is very vulnerable.

2008 Was A Warning.

This is a crisis waiting to happen. The IMF has said that one policy misstep would be enough to topple the very fragile global financial system. The Bank for International Settlements has said that the central bankers are out of ammunition to deal with the next crisis. They said this over a year ago, and things are only worse today.

The stock markets are breaking down and insiders are selling. The naïve public is holding or buying. The currency markets are unraveling their pegs.

In Lynette’s opinion, owning tangible wealth outside of the system is the most conservative move one can make in the current environment. She warns that there is only one tool left to deal with the situation and that is inflation. Chances are quite good but the central bankers will lose control of inflation as well.

The Crash Of 2008 Was A Warning : More Vulnerability.

Your stocks, bonds, and deposits are more vulnerable now than ever. Laws and contracts have been put in place, perhaps to insulate banks during the next crisis. Within the fine print in the account agreements at all of the financial institutions is a simple disclosure; once you deposit your funds into the financial institution you cease to have ownership of that wealth. All you really own is a contract that says that if they can perform they will but if they can’t you lose. Legally, you own nothing.

2008 Was A Warning.

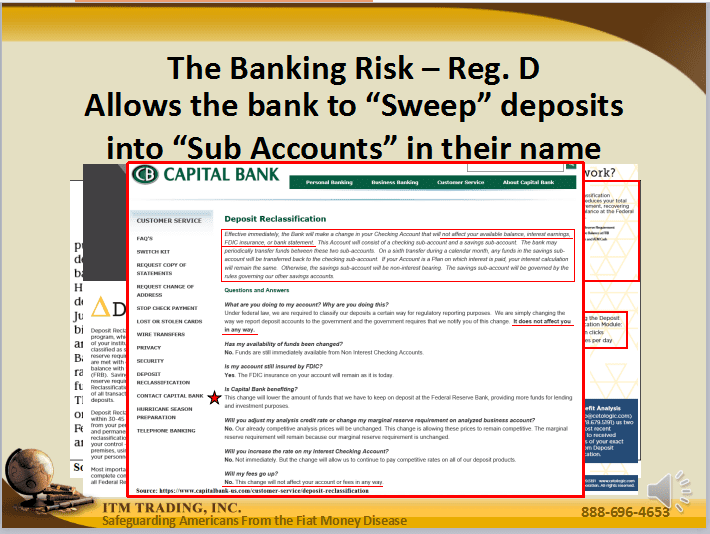

Bank deposits are governed by Federal Reserve regulation D. This states that once you deposit funds into any banking account the bank has the right to sweep those funds into a subaccount. This account is in the name of the bank and they can use it for their benefit. If a bank begins to fail, according to the Dodd-Frank act, the bank and convert your cash deposits into bank stock. Schemes such as this have already happened in Greece and several countries around the world.

Next, Lynette takes the opportunity to point out that the FDIC is insuring $10 trillion with $45 billion worth of funds. You can see how this won’t work. The global blueprint for banking failures is to bail in the taxpayer.

How Will The Banks Use Your Investment Account Money?

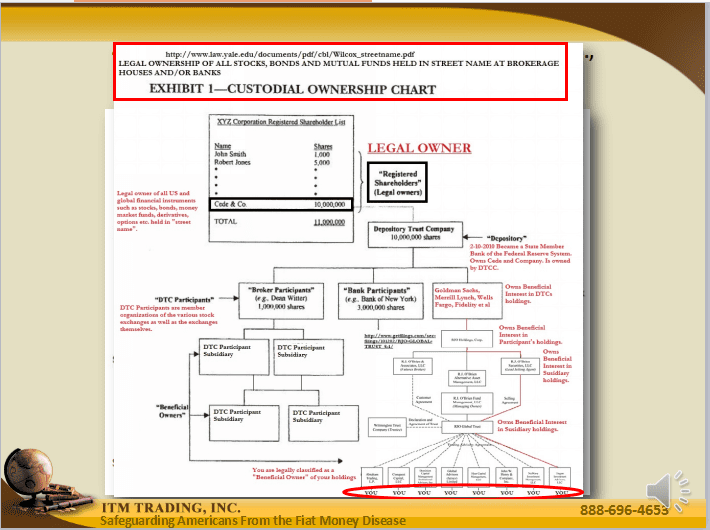

When you opened your brokerage account you entered into an agreement. All securities in your account are held in street name. You are the beneficial owner and Delaware Trust Company or DTC is the legal registered owner.

A recent Yale study examined the ownership structure of all of the fiat financial instruments. On the bottom of the structure is the beneficial owner, which is you. The benefit you have through your account is the ability to buy and sell.

2008 Was A Warning.

Cede and company, in essence, passes along any profit or dividend and creates the illusion that you really own something. Because all of the corporations and companies that hold your investments are interconnected, if one goes down they will all go down.

All of the companies below DTC are also classified as beneficial owners. This makes it legal for them to use your equity for their benefit. This is the reason you really don’t own a savings or investment account. By signing these banking agreements you agree to give away your wealth.

If you don’t hold it, you don’t own it, and you certainly don’t control it so therefore it is vulnerable. When a financial crisis hits your wealth will migrate to hidden depths and no one will be held accountable. The 2008 perpetrators were bailed out and given 0% loans to repay their debts to each other and no one went to jail. The same will happen again.

The Fiat Money Disease Opportunity.

Fiat schemes are about wealth transfer. You need to be able to identify wealth transfer opportunities. The big money is buying gold. Around the world, central banks are filling their vaults with physical gold. Lynette believes that the central banks are acquiring gold in preparation for a global financial system reset.

If a reset were to happen today, using the numbers of Jim Rickards the dollar value of physical gold is somewhere north of $8200. This is the valuation of all of the fiat money printed valued against the finite amount of gold. Being that spot gold is around $1130 an ounce right now, gold is severely undervalued.

Gold and silver are the foundations of Lynette’s strategy. The goal is to take advantage of wealth-building opportunities as the current fiat system dies. Gold and silver are a place to park your purchasing power until those opportunities arrive.

The manipulated spot prices of gold will really create opportunities in stocks and real estate. When the bubbles in stocks and real estate burst, deleveraging will occur. Prices will plummet. There will be bargains to be had.

IRA Approved Gold and Silver Coins and BarsÂ

The Crash Of 2008 Was A Warning : Conclusion.

Those that own gold and silver physically will have the wealth with which to purchase these bargains. This is just a part of Lynette’s strategy. Lynette closes her webinar by inviting you to call ITM Trading and discuss owning gold and silver as part of your portfolio with an ITM Trading representative. ITM Trading is here to be of service and will work hard to create a strategy tailored specifically for you and your goals. Call us at 1888 OWN GOLD to begin the discussion.

2008 WAS JUST A WARNING, FREE WEBINAR SERIES:

We will show you why The Great Recession of 2008 was just a warning.

Why the next financial crisis will be much larger than the Great Recession of 2008.

Watch this free webinar series and learn how to prepare, survive and thrive during the coming financial crisis.

Reserve Your Seat For Our Next Live Webinar Or View Recordings of Past Webinars – E-mail Us

Have Questions? Call Us Monday – Friday 8am – 5pm at 1-888-696-4653

What Webinar Attendees Are Saying:

Great presentation, Lynette!

Really clear and helpful…..Thank you so much…

Barb

———————————————-

Lynette,

Thanks so much for the education and the current events updates.I am enjoying the webinars!

Thanks,

Donna

———————————————-

Dear Lynette –

I’ve been on the past webinars, and your knowledge of what’s occurring in

the financial world is amazing. I’m very grateful that you’re sharing that knowledge.

Thank you.

Linda M