THE ILLUSION OF CHOICE AND SAFETY: When Washington and Wall Street Merge

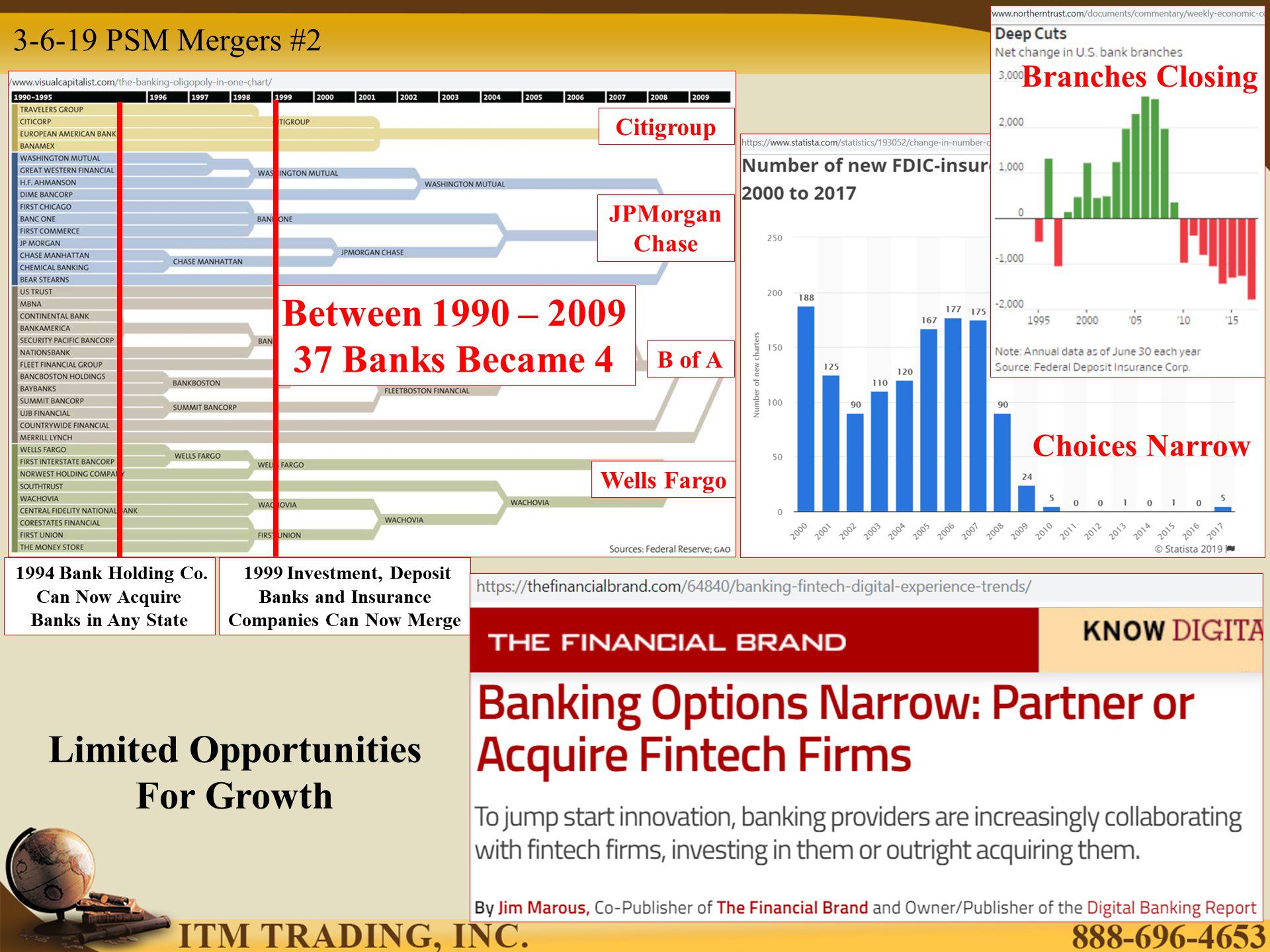

Confidence in the banking system is critical to the fiat money system, that’s why the FDIC insurance scheme was created in 1933, to restore confidence in the banks. Much like the Dodd-Frank Wall Street Reform and Consumer Protection Act bank, designed to instill confidence after the financial crisis that became apparent in 2008 and concluded a big bank consolidation period that began with the Riegle-Neal Interstate Banking and Branching Efficiency Act of 1994. For the first time, bank holding companies could acquire banks in any state.

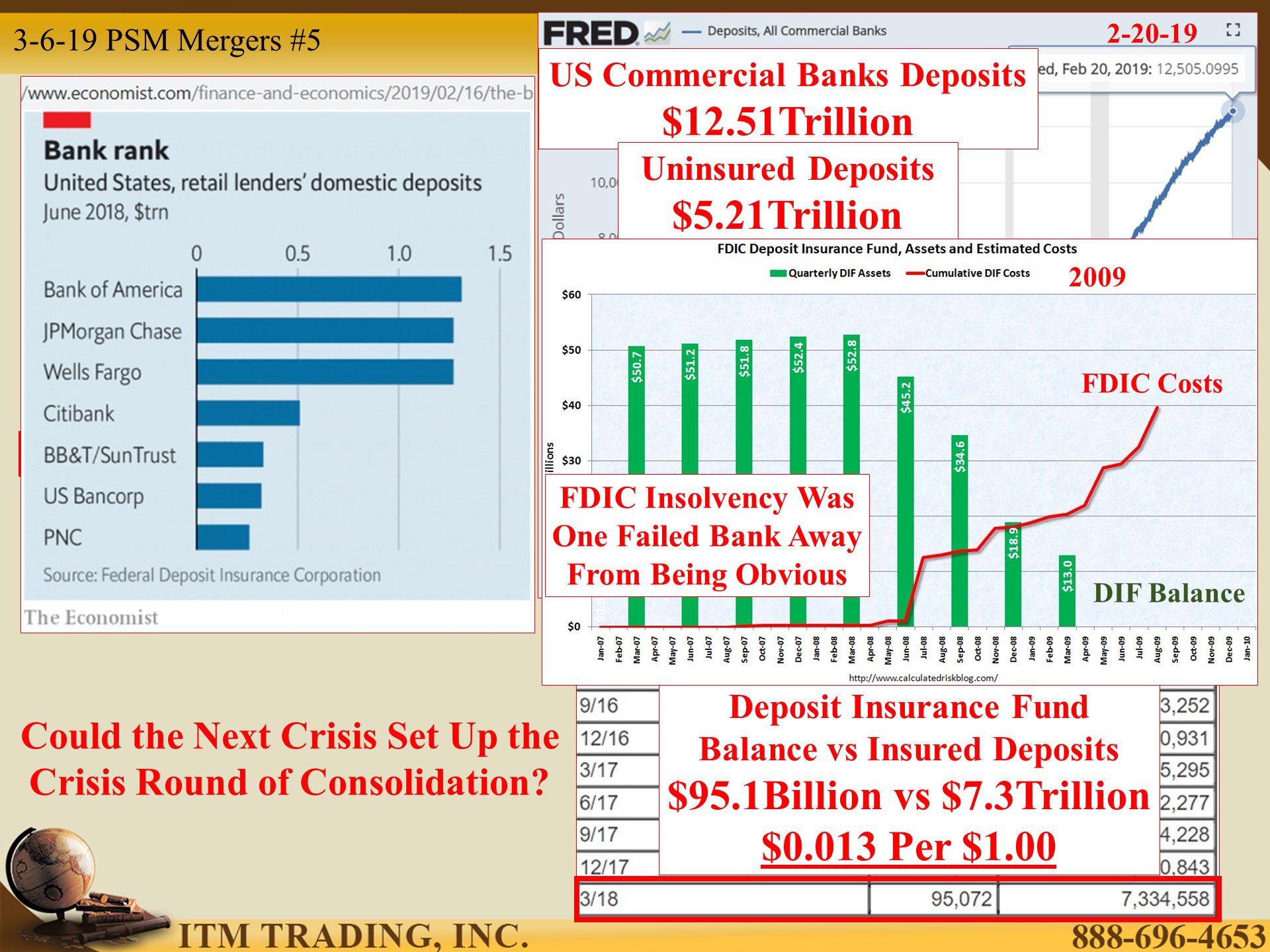

The result? In 1990 there were 37 large banks. In 2009 only four mega banks were left: JPMorgan, Citibank, Bank of America and Wells Fargo. That’s a considerable loss of consumer choice and created the Too Big Too Fail (TBTF) Banks that were bailed-out by the taxpayer and have become even bigger since as smaller banks have been gobbled up.

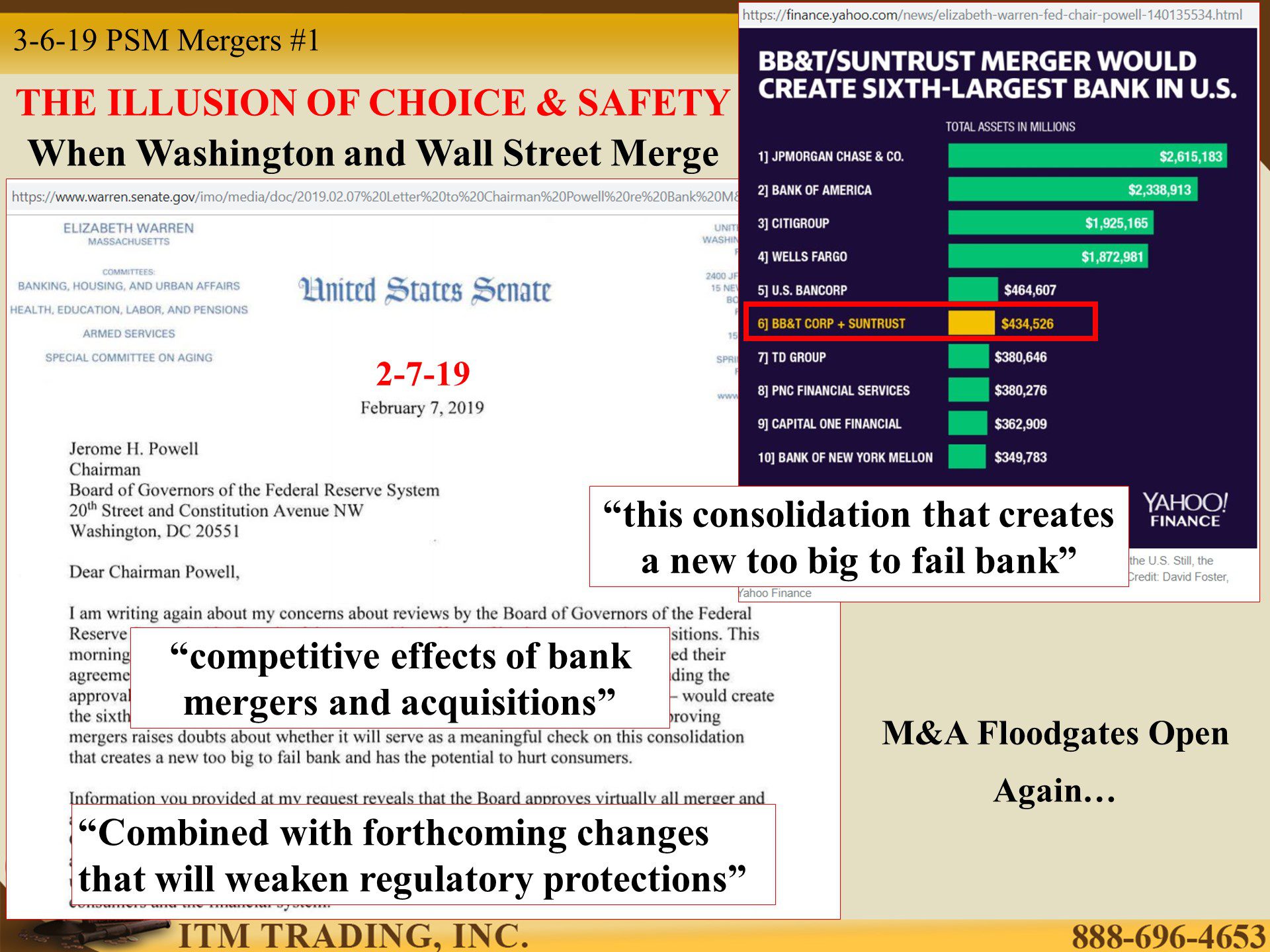

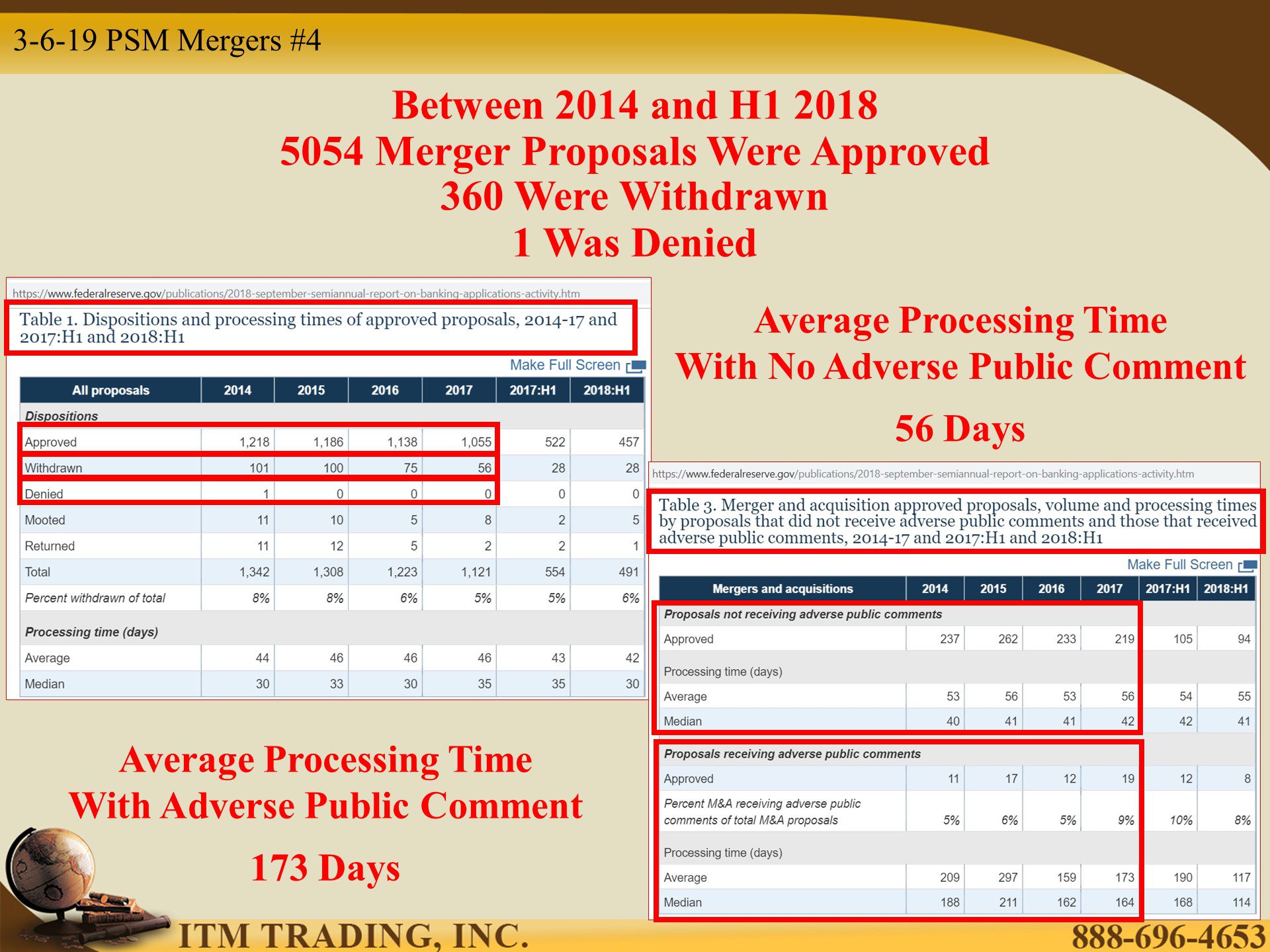

This has put into question the Federal Reserves policies surrounding bank M&A. According to the September 2018 Semi-Annual Report On Banking Applications Activity, between 2014 and the first half of 2018: 5054 merger proposals were approved, 360 were withdrawn and 1 was denied. Â When you couple fed policy with President Trumps bank deregulations that formally began in May 2018 which changed bank size requirements for regulation compliance.

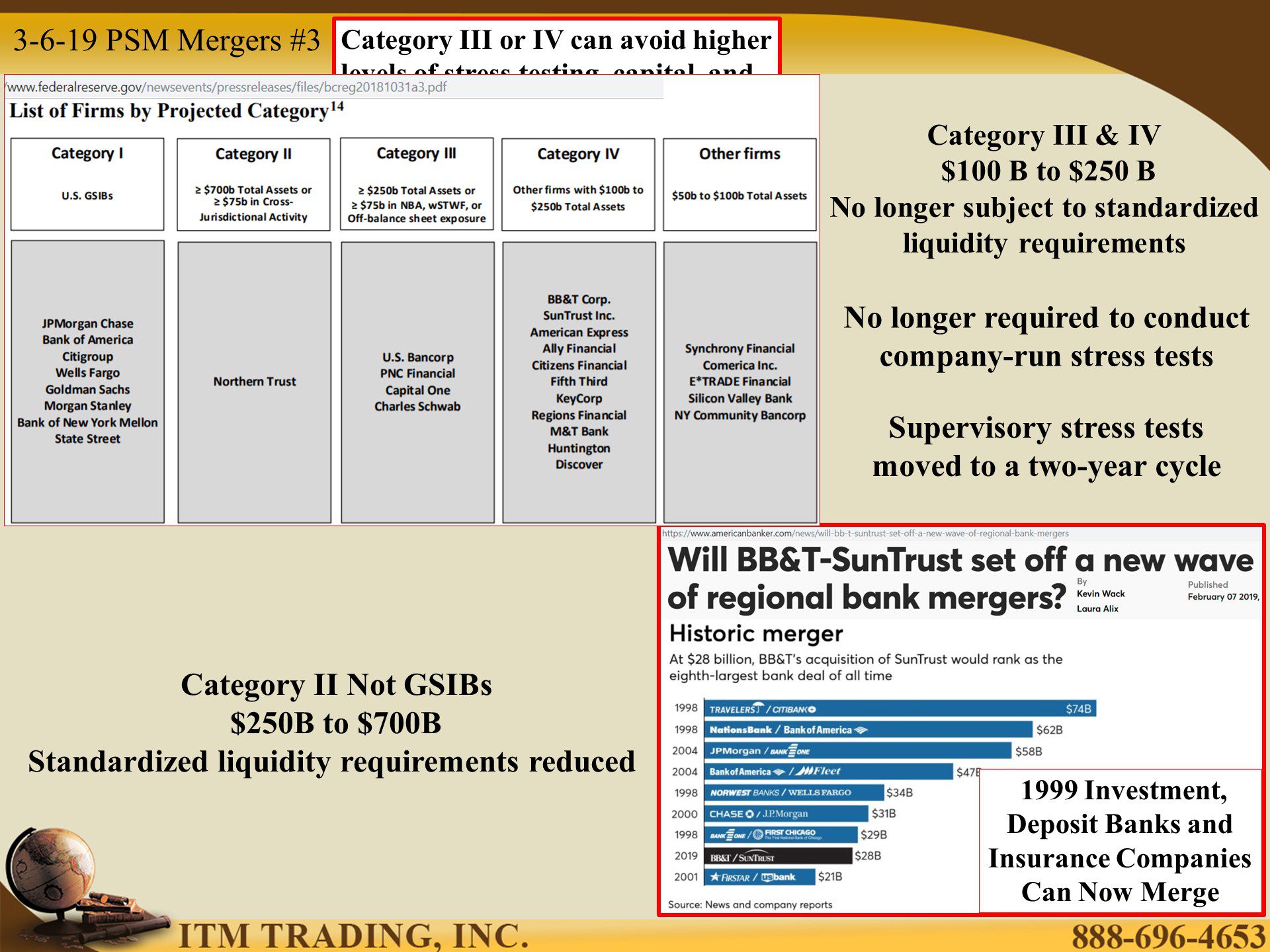

Today we’ll focus on those changes that impacts those banks below $250B and possibly encourages a rash of M&As in the smaller banks and may well create more TBTF banks, starting with the upcoming merger of BB&T and SunTrust Inc, with would create the fifth largest bank by deposits.

Why does this matter to you? Because the current changes lower levels of stress testing, as well as, capital and liquidity requirements putting YOUR deposits at risk.

Not worried because of FDIC insurance? Well, according to the most current DIF Report there are roughly $7.3Trillion insured deposits in the commercial bank system, but only $95.1Billion in the deposit insurance fund. That works out to $0.013 to insure $1.00. Not a problem if not too many banks fail at the same time, but in 2009, the FDIC was one failed bank away from their insolvency being obvious to the public, which would have nullified public confidence.

Do you think this might become obvious during the next crisis? I’m guessing yes and perhaps global central banks think so too. Today, financial gold accounts for more than a third of all above ground gold with a surge in the amount of gold buying as well as the number of central banks buying gold. It is clear they are building their shield in preparation of the next crisis. I am too, are you?

https://finance.yahoo.com/news/elizabeth-warren-fed-chair-powell-140135534.html

https://www.visualcapitalist.com/the-banking-oligopoly-in-one-chart/

https://www.fdic.gov/regulations/laws/important/

https://www.sec.gov/rules/final/34-49830.htm

https://thefinancialbrand.com/64840/banking-fintech-digital-experience-trends/

https://www.barrons.com/articles/federal-reserve-is-seen-helping-bank-mergers-51548943990

https://www.occ.gov/news-issuances/bulletins/2018/bulletin-2018-46.html

https://www.americanbanker.com/news/will-bb-t-suntrust-set-off-a-new-wave-of-regional-bank-mergers

https://www.govinfo.gov/content/pkg/FR-2018-12-21/pdf/2018-27177.pdf

https://www.federalreserve.gov/newsevents/pressreleases/files/bcreg20181031a3.pdf

https://www.visualcapitalist.com/the-banking-oligopoly-in-one-chart/

https://www.calculatedriskblog.com/

https://fred.stlouisfed.org/series/DPSACBW027SBOG

Today we’ll focus on those changes that impacts those banks below $250B and possibly encourages a rash of M&As in the smaller banks and may well create more TBTF banks, starting with the upcoming merger of BB&T and SunTrust Inc, with would create the fifth largest bank by deposits.

Why does this matter to you? Because the current changes lower levels of stress testing, as well as, capital and liquidity requirements putting YOUR deposits at risk.

Not worried because of FDIC insurance? Well, according to the most current DIF Report there are roughly $7.3Trillion insured deposits in the commercial bank system, but only $95.1Billion in the deposit insurance fund. That works out to $0.013 to insure $1.00. Not a problem if not too many banks fail at the same time, but in 2009, the FDIC was one failed bank away from their insolvency being obvious to the public, which would have nullified public confidence.

Today, financial gold accounts for more than a third of all above ground gold with a surge in the amount of gold buying as well as the number of central banks buying gold. It is clear they are building their shield in preparation of the next crisis. I am too, are you?