DON’T CALL THIS MMT: But if it Quacks Like a Duck…HEADLINE NEWS with Lynette Zang

I don’t know about you, but things are heating up and heating up and central banks are running out of options! After all, they’ve been zero bound and their balance sheets are huge. But let’s talk about that, because there’s a really recent report from the IMF just came out the other day that I wanna show you.

TRANSCRIPT FROM VIDEO:

Oh, oh, I’m sorry. I just feel so bad for these Central Bankers that are losing choices, but don’t worry. I think they have some other ideas, coming up.

I’m Lynette Zang, Chief Market Analyst here at ITM Trading, a full service, physical gold and silver dealer. Really what the specialty is, is to help people get prepared to sustain their standard of living and be in a position to take advantage of opportunities that present, because, I don’t know about you, but things are heating up and heating up and central banks are running out of options after all they’ve been zero bound and their balance sheets are huge. But let’s talk about that because there’s a really recent report from the IMF just came out the other day that I wanna show you.

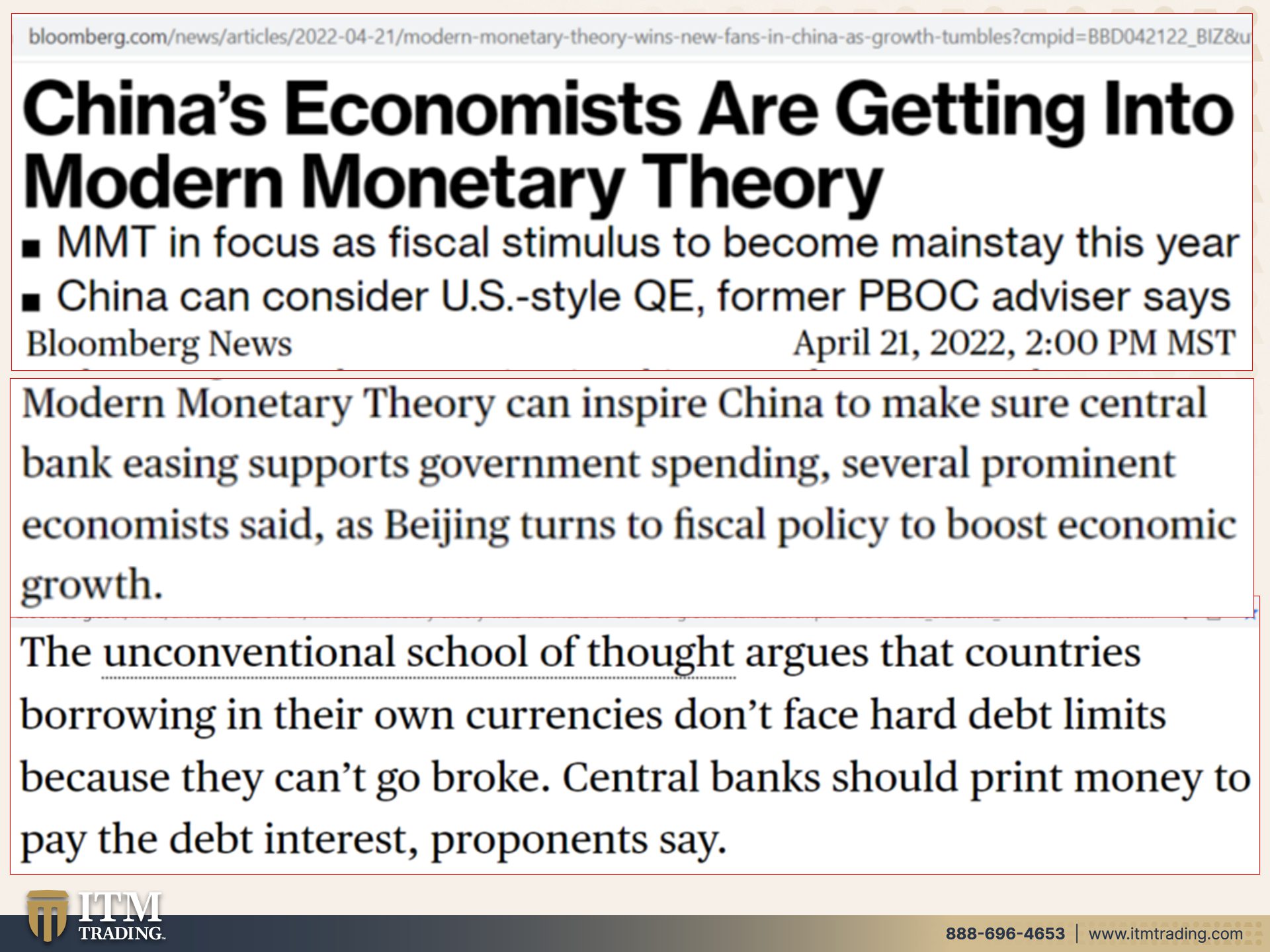

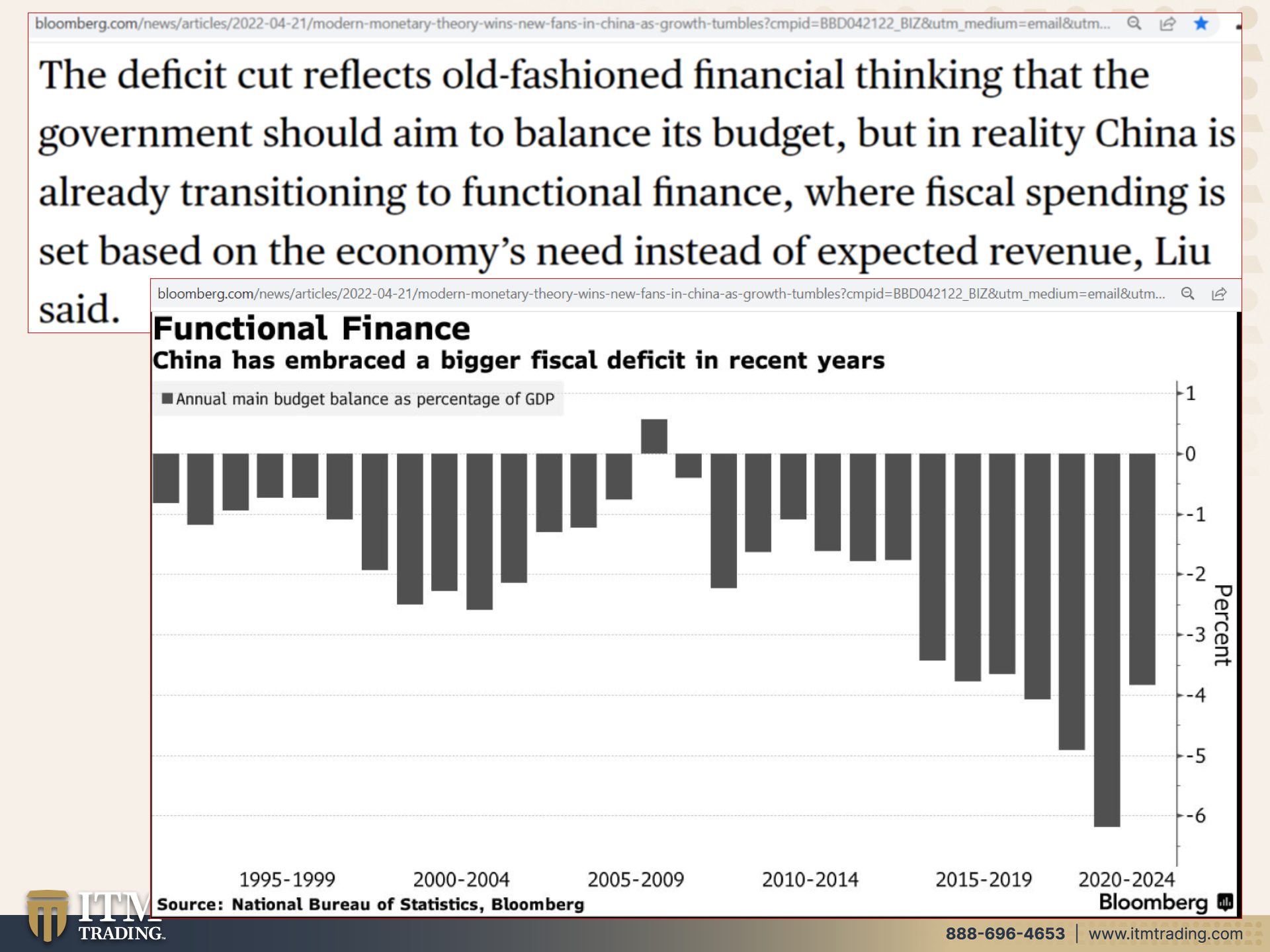

But first in kind of like let’s all help each other learn. Remember I’ve told you right along that there’s China is really teaching the world, the central banks, the governments, how to control the population and whether or not you realize that, our options and choices have grown more and more narrow over that time. And what have we taught China? Well, China can consider us style QE. Well, okay. Just print, print, money, modern money theory, even though they don’t admit to actually doing it. This is really what the central bankers have been doing since 2008 Modern Money Theory can inspire China to make sure Central Bank easing supports government spending. Except what they don’t tell you is that every single time, no, which one’s that one every single time they do this, whatever is out there loses value, but hey, insanity is doing the same thing over and over again and getting the same results. You know, are we gonna get different results? Probably not, but they’re gonna try to do that. To boost economic growth. All they will boost is inflation. The unconventional school of thought, which has become convention, really argues that countries borrowing in their own currencies. Like the U.S. Don’t face hard debt limits because they can’t go broke. Central banks should print money to pay the debt. Interest proponents, say what say you? I say, nay, this is what we’ve been living through. The deficit cut, reflects old fashion financial thinking, wow, you should balance your budget. How about you? And I just take some credit cards and go out and spend and spend and spend. And then when we’ve maxed out those cards, we could tell the credit card companies, we’re just doing what the central bankers are doing. That’s old fashioned thinking that you think I have to pay that bill. My goodness in reality, China is already transitioning to functional finance where fiscal spending is set based on the economy’s need instead of expected revenue. Hmm let’s see. I have heard my kids say many times that they needed a new bike or they needed a new toy. Do you really need it? Or was it that you wanted it?

You need Food, Water, Energy, Security, Barterability, Wealth Preservation, Community, and Shelter. That’s what you need. But forget all of that because as we know, it is very easy to spend other people’s money. And when governments spend taxpayers money, that’s exactly what they’re doing. And it’s very easy thing to do.

Now I have to, I have to tell you, this was probably a mistake Juliette here, but I got the newest member of our security team, cause you know, that’s a big one and I, she wanted to come in and sit with me, but she’s kind of making noise. Are you coming over here? Juliette Juliette here, here. So meet, meet the newest…Edgar’s crawling meet the newest member of our team. Little Juliette. She is a little six month old. Great Dane. So she’s not so little 67 pounds, but she’s a very good girl. Most of the time. Not all the time yet, most of the time. Okay.

So this is Functional Finance, forget deficits. Who cares? Except here’s the problem. Whether you are a government, a corporation or an individual, ultimately the laws of finance or actually nature’s law of economics. It always ends up the same way. You can’t just create something new or spend this much money and expect everything to be hunky dory. Nothing’s gonna change. Are you kidding?

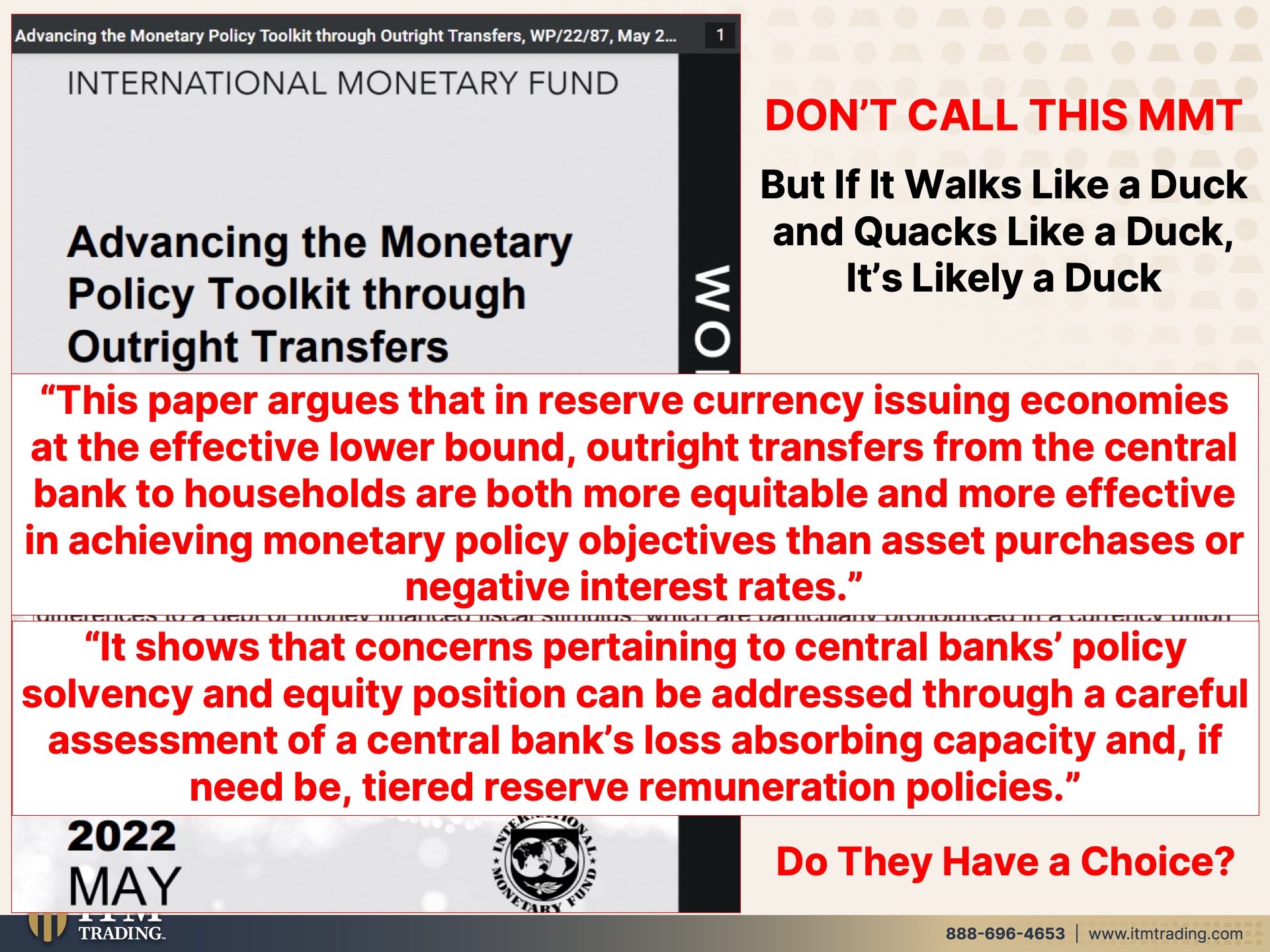

But don’t call what we’re doing here MMT Modern Money Theory. However, I really do believe if it walks like a duck and it talks like a duck and it’s, and it lays eggs like a duck. Yeah. It’s probably a duck. But since they’re running out of tools, let’s create a new one. Now we’ve kind of been talking about this for a while, but don’t call it MMT. Let’s call it Outright Transfers. So a lot of people have asked me how the central bank will get the CBDCs into the people’s hands. And this is actually perfect for that.

This paper argues that in reserve currency, issuing economies at the effect of lower bound. In other words, with zero interest rates, that’s what effective, lower bound is, outright transfers from the central bank to households are both more equitable. Oh see, those transfers are more fair and more effective in achieving monetary policy objectives than asset purchases, which they’ve been trying since 2008. And it hasn’t really stimulated the economy or negative interest rates, which they’ve also been testing since 2009. So they’re admitting that these things aren’t working. Wow, that’s pretty amazing. So now we’re gonna try something else with outright transfers or OT. It shows that concerns pertaining to central bank’s policy solvency and equity positions that they create these things out of thin air, can be addressed through a careful assessment of central bank’s loss absorbing capacity. It’s really all based on confidence and trust, and if need be tiered reserve renumeration policies.

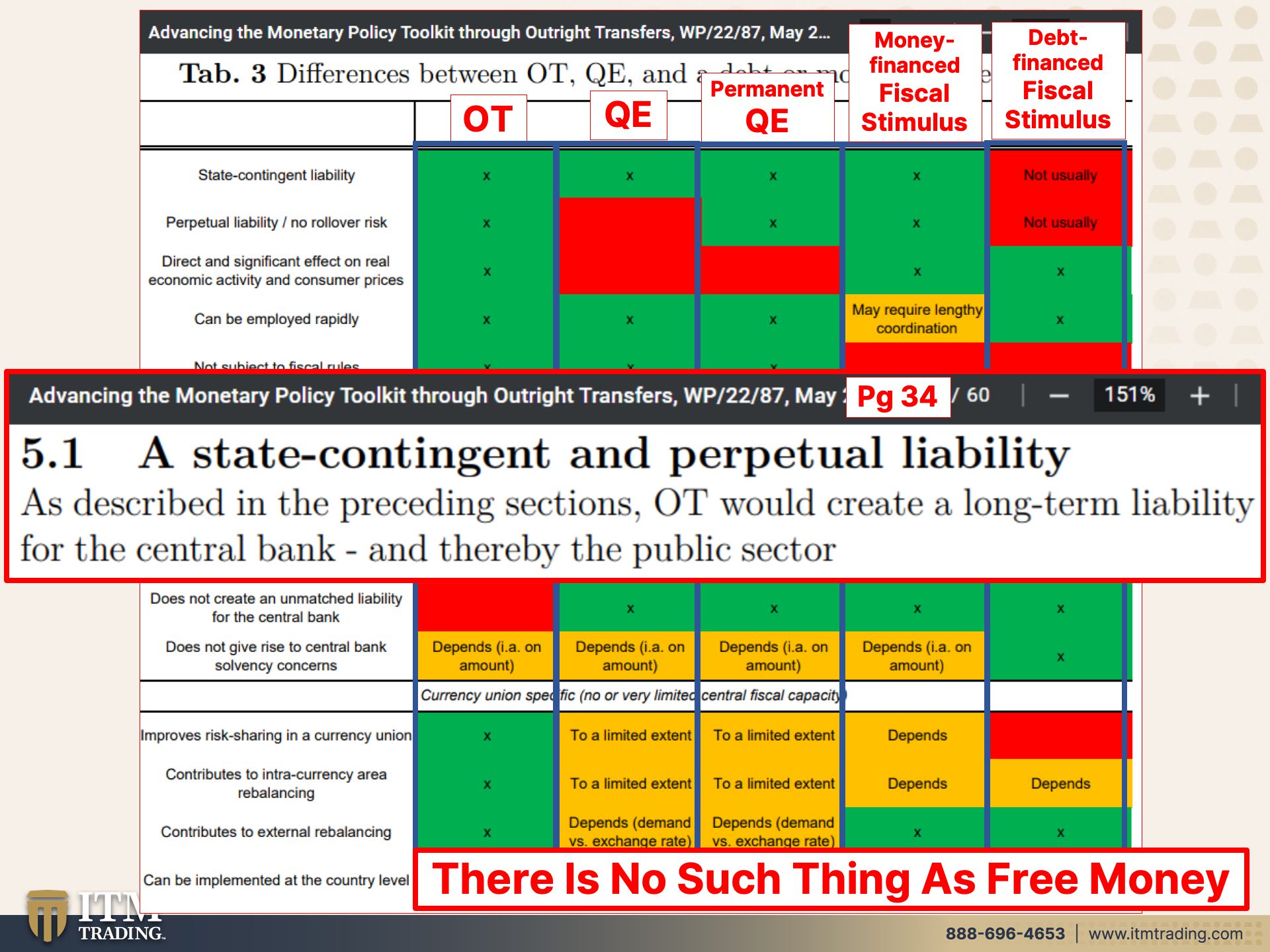

So in other words, they create this debt at a thin air and that’s the, that’s the Chinese central bank, but we’re doing the same darn things doesn’t really matter. And then we have the interest, the taxpayers have the interest on that debt to pay that’s the reserve renumeration and tiered meaning. You can have different levels of that. So my bet would be that the corporations get it the cheapest, but the public it’s gonna cost more, shocker! That’s the way they always do it. But really, the question is, do they have a choice? They’re throwing anything on the wall to see what will stick, but I love this little colorful graphic on the different programs that have attempted. So here’s the OT that we talked about and wow! Look at how much green is in there. Now it does not give rise to fiscal dominance risks. So not for moderate amounts, but if you do enough, you’ll have more risk with that. And it does not create an unmatched liability for the central bank, really? So they can just create this and there’s no attached liability, get your money for nothing and your chicks for free. Yeah. and it does not give rise to central bank solvency concerns. In other words is a central bank solvent? Well, Hey, if you can do this, why would you not be solvent? Because every single time you do that, what you put out there destroys a layer of confidence because it feeds into inflation, particularly in this environment. I think the timing of when they put this report out is kind of interesting since they were looking at a low or what they considered a low inflation environment. So there’s OT now there’s QE, there’s permanent QE. Did you know there was a permanent QE? Cause yep there is. And money financed fiscal stimulus as well as, as well as debt financed, fiscal stimulus. So you can see which one has the most green? Oh, the OT, the new tool. But while they’re saying that it’s not a liability for the central banks, a state contingent and perpetual liability as described would create a long-term liability for the central bank and thereby the public sector, meaning it is a liability for the taxpayers for you and for me. So one thing that I found really interesting in these reports, and of course you have the links, so you can go and read them for yourself is how often they contradicted themselves. Because here they’ll say, well, it doesn’t create a liability for the central bank. And then in the next chapter they say that was tab three. This is 5.1. They say, yeah, it’s a liability. And I actually found that quite a bit during, or while I was reading this whole piece. And the reality is there is no such thing as free money. Inflation is the cost of that money. Interest rates are the cost of that money. And while central banks can buy debt and push down those costs, they haven’t eliminated them. They have merely pushed them into the future. And guess what? The future is here. You know, you can only kick a can down the road for so long and they’re done.

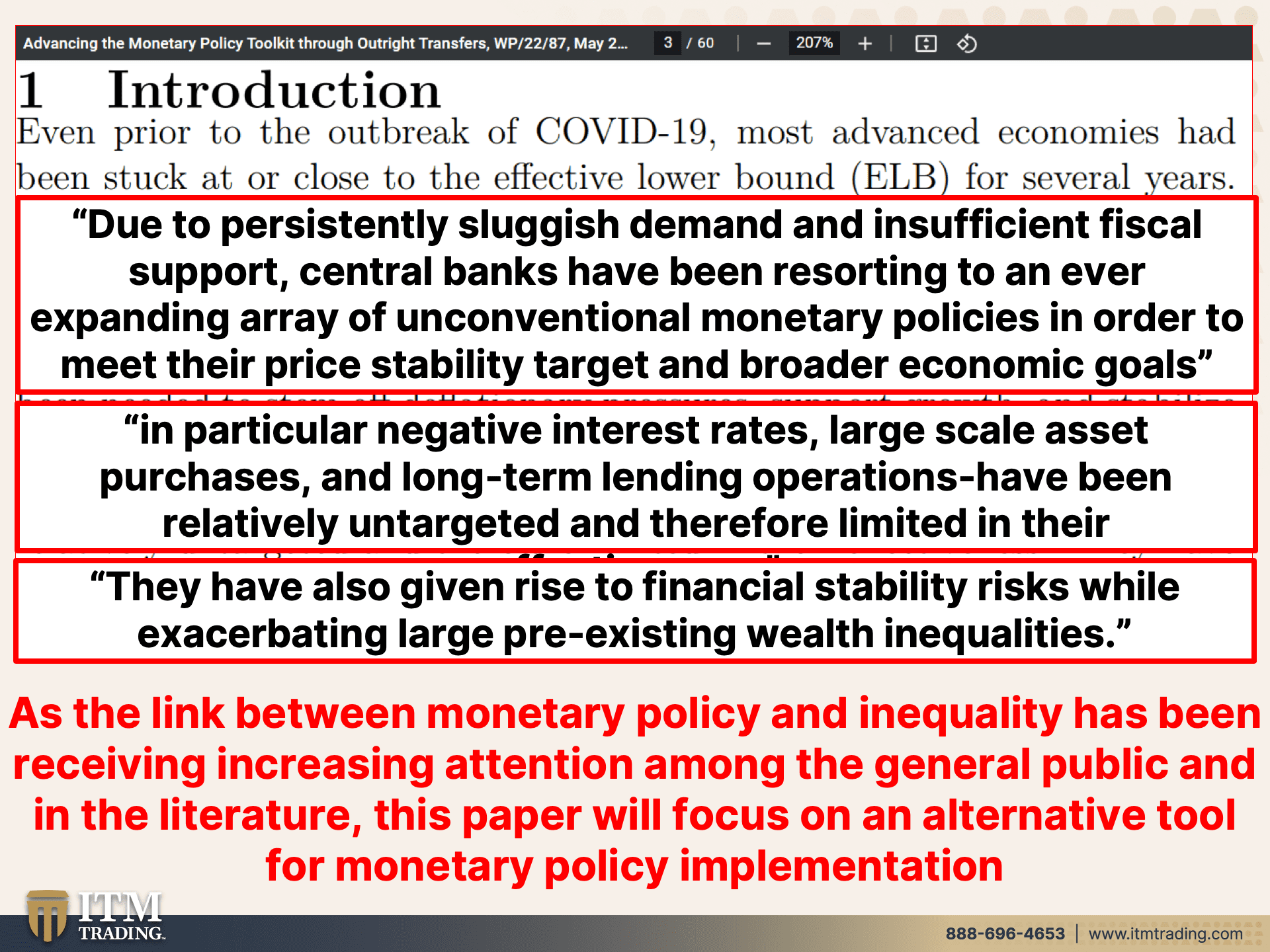

But this is even prior to the outbreak of COVID 19, most advanced economies had been stuck at or close to the effective, lower bound. In other words, zero interest rates and interest rates are the single biggest tool of central banks to regulate the rate and speed of inflation. Right? So now they have to raise rates. It’s gonna be really interesting to see how many times they raise them before they’re forced to turn around and lower them again. They gotta do it for their credibility, but due to persistently sluggish demand, wait a minute. They’ve been telling us how great the economy is doing and how great the consumer is doing, due to persistently sluggish demand and insufficient fiscal support. Are you flipping kidding me? Central banks have been resorting to an ever expanding array of unconventional monetary policies in order to meet their price, stability, target, and broader economic goals. What is price stability? It is the price at which you, the worker, you don’t really pay any attention to inflation and therefore you don’t ask for an increase in your wages, but frankly, that’s come to an end it’s over. So that means price stability is over. And that means more people are going to lose confidence in the central banks and in the monetary system, money for free? Yeah, of course they’re gonna take it and they’re gonna spend it. But what we’ve seen is when governments do that, they spend what’s in there. But if you expect them to then start depositing and using that same system, they’re not so cooperative. Yeah they’ll take it for free why not? I mean, you’re gonna do that aren’t you? In particular negative interest rates, large scale asset purchases. So all the bonds that, that the central banks have been buying and long term lending operations have been relatively untargeted. Yeah. They’ve been very targeted as in that K-shaped recovery. I’d say they’ve been very targeted to help the wealthy, get wealthier and to transfer that wealth from those that are on a lower level, 90% of the bottom, that wealth has transferred to the top. So that’s why it’s been limited in their effectiveness. Are you kidding me? Look around you. Stock market bubble is bursting. Bond market bubble is bursting, real estate market there are signs of it bursting, but not as big signs as the stock markets and the bond markets, but this was an over target for reflation. And I would say that it was very targeted and also very successful, unfortunately, but did it trickle down to the masses? No. And frankly, they’ve known that trickle down theory does not work and they’ve known it for a really long time. They have also given rise to financial stability risks while exacerbating large pre-existing wealth inequalities. Okay. They’ll give you that, they’ll admit, but they don’t really say this was our fault because no let’s point the finger. It’s all their fault. It’s their fault. It’s your fault. You gotta go out and spend, spend, spend not our fault. Mm-Hmm <affirmative> as the link, but here’s the kicker. As the link between monetary policy and inequality has been receiving increasing attention among the general public and in literature, this is what they don’t want. They don’t want you to realize what they’re doing and they are, people are waking up. Maybe not as fast as some of us would like. I mean, frankly, I’d like everybody to be awoke right now, but people are noticing that’s the problem with rapid inflation and high inflation is people notice let’s see, this paper will focus on an alternative tool for monetary policy implementation.

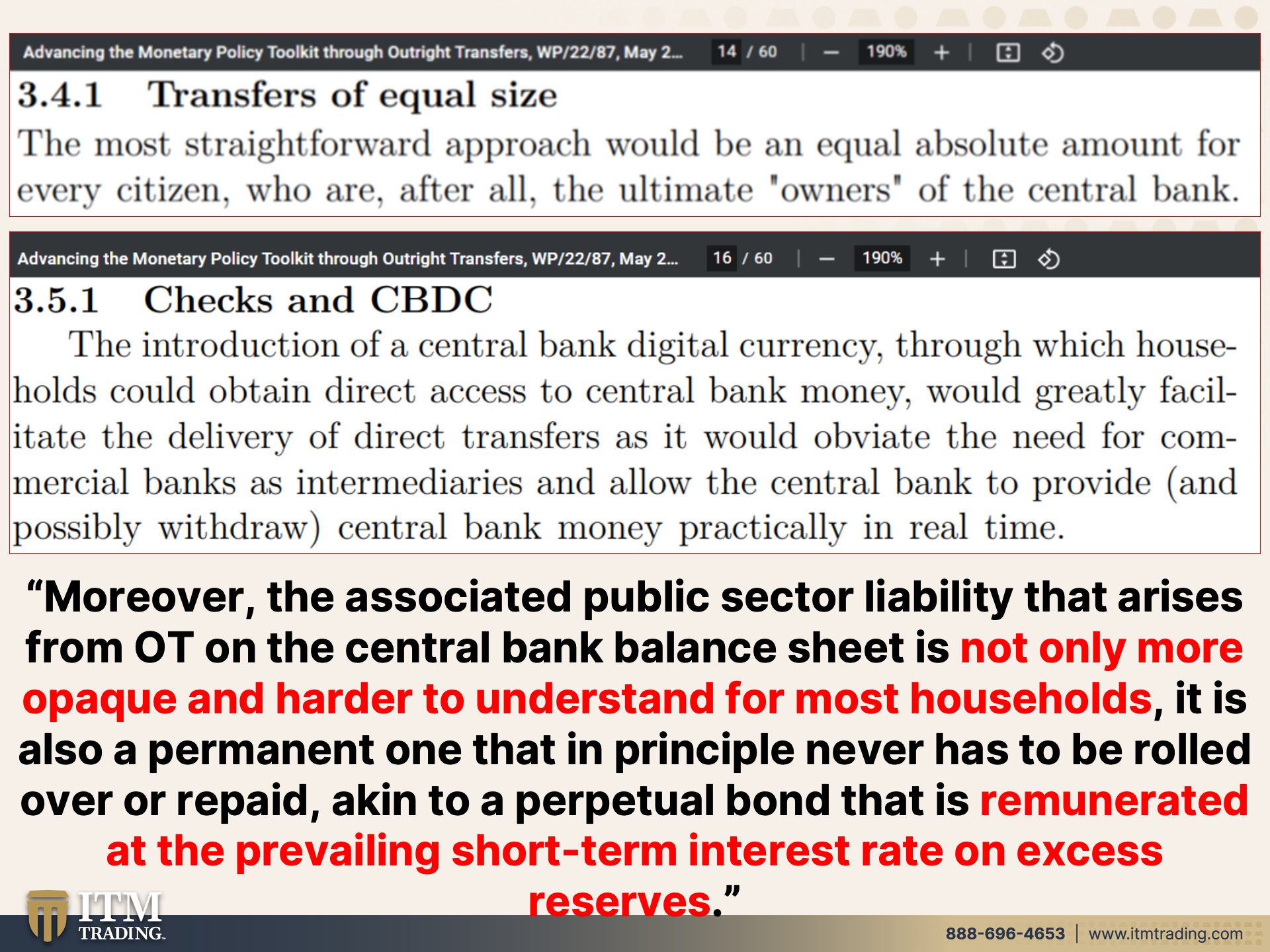

Well, let’s take a look at what that alternative tool is, outright transfers. So there are a number of ways in which they could do it, but the most straightforward approach would be an equal absolute amount for every citizens, who are after all the ultimate owners. How about we of the central bank? How about we say the ultimate at risk entities of the central bank’s actions. Yeah, here they admit it. We’re the owners of the central bank and that’s why we have to pay for the liabilities. Are we benefiting from all this money printing? No, we have a K-shape recovery, right? And we’ve seen that wealth and income inequality have been stretched and stretched and stretched since when was that? Oh, the 80s as this big experiment after we were taken off the gold standard, started to progress and expand with the central banks in control. Let us not forget that please, further, checks and CBDCs. So how are they going to distribute these transfers of equal size? Which by the way, sounds like universal basic income to me. I don’t know, they don’t use term in here, but they don’t use modern money theory either. But again, walks like a duck quacks like a duck and lay eggs, like a duck? It’s a duck, probably so. Okay. The introduction of a central bank digital currency through which households could obtain direct access to central bank money. Remember the fed now accounts, everybody already has an account set up, already, even though the CBDC’s is not ready. Well, let’s put the cart before the horse or maybe not, maybe it’s ready and they aren’t just telling us that yet. Maybe it’ll magically appear ready during this next financial crisis that could frankly happen anytime. Okay. Let’s see. Access to central bank money would greatly facilitate the delivery of direct transfers as it would obviate the need for commercial banks as intermediaries and allow the central bank to provide and possibly withdraw central bank money practically in real time. Yeah, we all have those accounts. So the central bank giveth and the central bank can taketh it away. You’re not spending it fast enough. Hey, this is programmable money, we can make it evaporate. We can set it up so that you can only spend it in these places. Frankly, if the central bank decides to give me money, if I have the ability to do so, I’m buying gold and silver with it. I’m converting that garbage into something real, real money, real money.

Moreover, the associated public sec. This is really listen to this. I’ll read it twice. Moreover, the associated public sector liability that arises from OT on the central bank balance sheet is not only more opaque and harder to understand for most households. It is also a permanent one that in principle never has to be rolled over or repaid, akin to a perpetual bond that is enumerated at the prevailing short term interest rate on excess reserves, which is by the way, controlled by the central bank.

Don’t change behavior, change the way you account for it so that people don’t understand what’s happening. How many times can you be lied to when you do not know the truth? Every single time and they have to hide it and hide it and hide it. Because if we really understood, if people really understood if how money was created and supported the full faith and credit of the central bank. So as long as you trust them, you have faith. Then you’ll keep loaning them money. You’ll give them credit. And if they can set things up so that you don’t understand, what’s really going on, so much the better they have you by the cajones, but I’m trying to show you what’s going on and what their intention is and what their plan is so that you can make educated choices that take you out of their system out, out, out, and holds its purchasing power value, short term, they can do anything but long term, that’s when you can more see the truth, but that’s why they have to suppress the price of gold and the price of silver. It’s ridiculous because they’re talking about an infinite amount of fiat and not just here, but like everywhere, everywhere, and not just in these two countries, but hey, why don’t they do it in Europe? I mean, everywhere they are doing it everywhere. You want something that’s unlimited and controlled by the guys that got us into this mess to begin with? I don’t, this is why this is what I do. Physical gold, physical silver plus Food, Water, Energy, Security, Community and Shelter, get it done, get it done.

They are outta tools and they are setting up the hyperinflation because what’s gonna happen. They raise the rates, these over inflated markets start to implode. How low will they have to go before the Fed’s gonna turn around and turn on those money spickets and if you think what they did in 2020 was a lot? Chunk change, just like what they did. I mean, when in 2008, it was, everybody was a gassed at that amount that they put into the system, nothing, nothing compared to what they did in 2020, this next pivot is gonna take us into the hyperinflation because what they’ve done so far will be dwarfed. Will they give everybody money? They have to, this is a consumer driven economy. They have to give people this money to spend because we don’t want the corporations to lose their massive profits that we’ve been watching. They’ve been taking advantage of this and gouging it. So the little bit of money that the government gave to the general public, well, you know, free money, easy in, easy out. And they say the consumer’s so healthy? hmmmmm I’m not so sure about that, frankly. I don’t believe them.

And Lo asks, what’s the solution? Perfect timing. You want to be as independent and self-reliant as possible. And you can get that faster. You know? I mean, basically I did it. I can’t say I did it on my own because I didn’t, I have had a lot of help over the last 12 years, 10-12 years that I’ve been working on this urban farm and I was buying gold and silver really as my foundation, before that, because this will put you in a position that whatever you don’t manage to put together before you absolutely need it, you’ll be able to buy it. If you don’t have the gold and silver, it’s gonna be a lot more challenging. So that’s why gold and silver needs to be the first step and the foundation because we’re running outta time. I mean, I really, I started accumulating a long time ago, many years ago, but doing the Food, the Water, the Energy, the rest of those pieces, it was after 2008 when I knew the system died. And I know what it looks like. You know, I’m not an expert in everything and I’m not ever gonna tell you that I am, but I don’t know anybody else. That’s been studying currency and currency life cycles since 1987. I don’t know anybody else that has. That’s what I’m an expert in. How do they make these transitions? And they give you stuff. They let the markets fly so that you buy into it. There are things that I’m told not to say because people have made a lot of money. Well, guess what? We had the roaring 20s and that hid all of the new money that was created by the central banks to kick this whole big experiment off. And, oh, let’s see. How about “greed is good” in the 1980s, as we transitioned from a gold standard to a debt standard and oh, by the way, what’s been happening in the 2020s up to this point or up until relative the beginning of this year? let’s say the first two years that K-shaped recovery, but people were given a whole lot of money. So for the CBDC’s and this Outright Transfers, sure, push a button, create a whole bunch of digits in an account it’s on your phone. Now that may be limited where you can spend it, but look at that money that we put on your phone and we’ll put the same amount in everybody’s account every single month. And oh, by the way, if you have kids, they’re gonna get some too. So let’s have a baby boom, because that’ll make sure that everybody gets more money. The problem is, is that it’s purchasing power value will be at bubcus a big fat zero because that’s what happens a hundred percent of the time. And insanity is doing the same thing and expecting different results. And maybe they aren’t expecting different results? Maybe they’re setting us up for this crisis so that when people are so scared and so desperate, they’ll hold onto any crumb that has offered them and then they gotcha. So what’s the solution? Get out of the system as much as you can, because I can always convert this into any Fiat, anywhere in the world at any time. Why? Not cause I say so, but because this has the most functionality in the broadest base of buyer and when you’re in crisis circumstance, what do you want? You want one buyer that buyer goes away, you’re left holding the bag or do you want 20 buyers? And they all need it. That’s what you want. That’s why gold has never gone to zero because it’s used across the entire global economy. And that’s why governments and central banks hate it because they know all of this and that’s the solution. Plus start a garden!

Make sure, I mean, I just did it, we’re gonna release it on Thursday, Friday, right? I just did an interview this morning that you guys are going to absolutely love it’s with Kristina Smallhorn and she is a real estate person. And the first part of it, we talked about a lot about what’s going on in real estate. So this is definitely a real estate focused video. But then on the second part of it going into BGS, we’re talking about shelter and we’re talking about all different kinds of shelters and tiny homes, etcetera. So you wanna definitely watch that because we’re talking about solutions, we’ve got a problem. The solution comes together in the Community. Can we go back to the slide please?

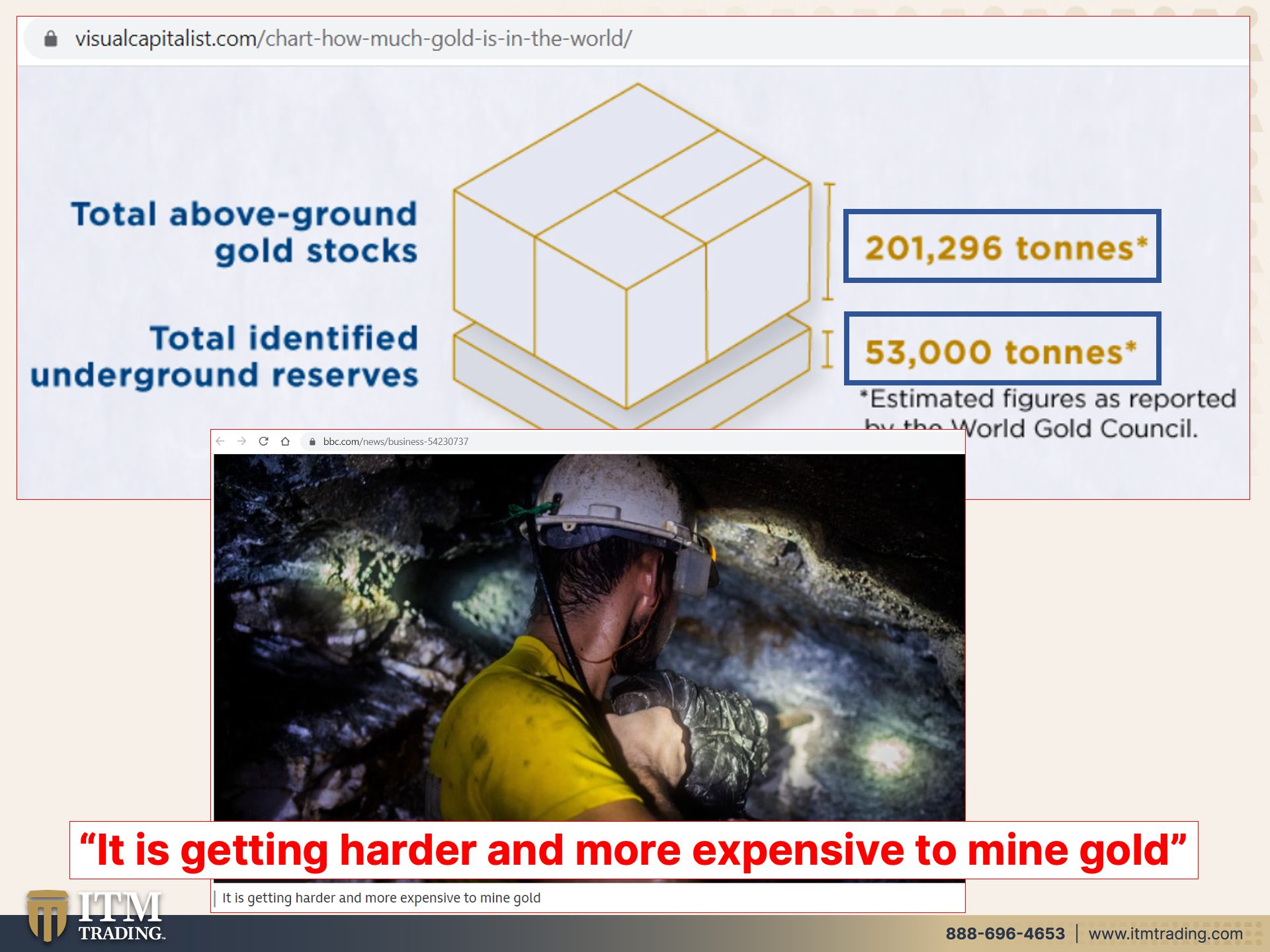

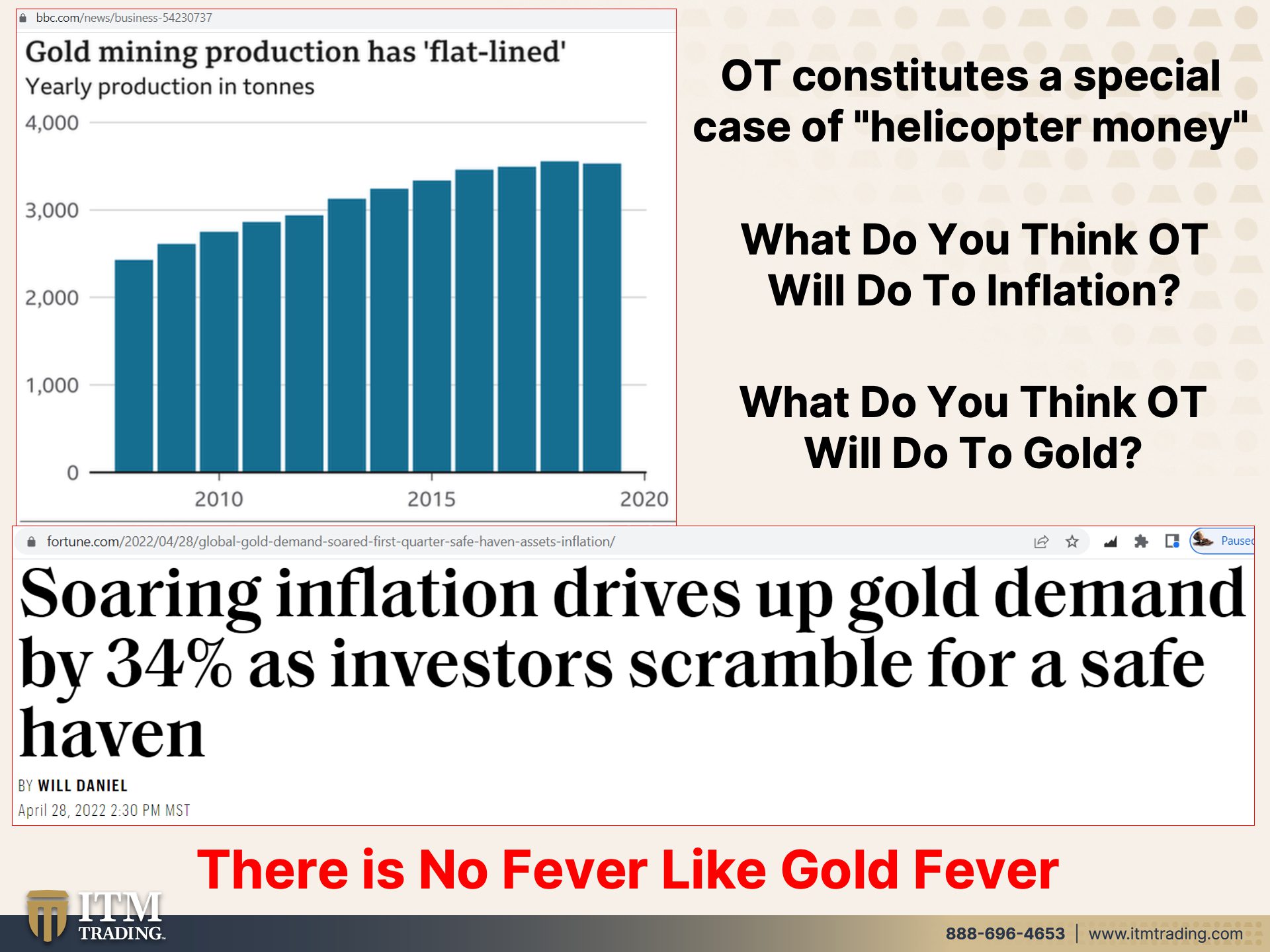

So let me show you one, one more little thing here, which is gold, right. In the physical world. I don’t care what it is, there’s a finite amount. If they find more of it? There’s still a finite amount of it. It doesn’t matter. There’s an infinite amount of this garbage because this takes nothing to create. That’s a button push. This takes labor and effort to produce. There’s almost 202,000 tons of gold that has already been mined and gold is recoverable. There’s another 53,000 tons that we know about or we estimate is yet in the ground. That’s it. We have already hit peak gold and central banks are buying it hand over fist and it’s getting harder and more expensive to mine gold. So that puts a floor underneath the Fiat money price, because they’re not gonna mine it and lose money on it. It’s not gonna happen. So let’s kind of take a look at this and do a little comparison because outright transfers constitutes what they call a special case of helicopter money.

And what do you think all of this money for free will do to inflation? Not gonna impact it? Wrong, wrong, wrong, something that is free. Well, that’ll go to its fundamental value too, which is a big fat zero. And therefore all of those financial assets that you might still be holding in your 401k in your retirement plan, you know, in your brokerage accounts, a trillion times, zero is ah, zero. So don’t be blinded by the numbers because they’re designed to, to direct you or nudge you in the direction that they want you to go in. But what do you think that outright transfers will do to gold when people lose confidence? Because mining production has flat lined. There’s a finite amount of it. And soaring inflation drives up gold demand by 34% as investors scramble for safe Haven. It’s not just the inflation. It’s all the very scary things. All of the things that are going on around us. So people are moving into gold. So they continue to suppress the price. I mean, right now we’ve got everything down in the markets, stocks, bonds, except gold is not down. I mean it is today, but for the year, no it’s up marginally. But I want you to also understand that that spot gold is a Fiat money product. That’s easy to control.

I’m not counting on wall street to tell me what the value of gold or the value of silver is. I have history as a guide. That’s a much better guide and this is a much, much safer place for all of us to be what’s the solution? Start a garden, make sure you have shelter, a place to go, maybe out of the maddening crowd, or even if you have to do it where you are Food, Water, Energy, Security, Barterability, Wealth Preservation, Community and Shelter and Community is arguably the most important part of it. Really? Because if you come together in Community, you have different knowledge base, you have different skill sets. You have different things that maybe you have stored. So if you don’t have a Community around you, well, that’s what we’re working on with Beyond Gold and Silver, is to help you meet you wherever you are in this process. But I’m gonna tell you, this is not the time to lolligag. This is not the time to procrastinate. This is the time to get it done.

I want you to definitely watch my interview that I did with David DuByne on our Beyond Gold and Silver channel. Our topic is on “Preparing for the Climate Change Crisis & Cooling Cycles” that he sees. And today, again, I had that interview with Kristina Smallhorn. I love her. I love David too. I mean, I’m really lucky that I get to spend time with such high quality and smart, smart, smart people. Part one will be out with Kristina part one will be out on Thursday on the ITM channel and part two on Friday on the BGS channel. You don’t wanna miss either one of those interviews. I view them very critically important and I’ll tell you what David DuByne over the years has been very influential on me. He’s the reason why I have indoor grow areas, frankly. Smart, smart, smart, smart, brilliant, man, brilliant. If you haven’t done it already, you definitely need to start your strategy. Gold and silver as the base, but you need everything. So if you haven’t set up a strategy yet, give us a call or click that Calendly link below and set up a time and please don’t don’t wait. This is not, things are not gonna get better. You know, they may appear to get better for a heartbeat of a minute, but we are in such a critical time right now. Get it done, please. And if you like this, give us a thumbs up. Make sure you leave a comment, cause it helps spread the word. And by the way, share, share, share. That’s so important and so critical because without a doubt, it is time to cover your assets. And until next we meet, please be safe out there. Bye bye.

SOURCES:

https://www.visualcapitalist.com/chart-how-much-gold-is-in-the-world/

https://www.bbc.com/news/business-54230737

https://fortune.com/2022/04/28/global-gold-demand-soared-first-quarter-safe-haven-assets-inflation/