IMF’s Map of Stagflation: This Is Keeping the Central Banks Awake at Night

We are living in a world where it’s easy to find a lot of doom and gloom as inflation continues to ramp up, and in my previous videos I covered the headlines of an upcoming housing market implosion. But everything doesn’t have to be about doom if you’re prepared. Which is why I’m getting my viewers ready to this so it can be situation for you to thrive when the world is in decline.

The IMF just came out with their 2022 Global Financial Stability Report, and there’s a shocking update that I am going to share with my viewers today!

CHAPTERS:

0:00 Video Overview

0:51 Intro

1:49 Growth Projections by Region

3:21 This Keeps the Central Banks Awake at Night

15:52 The Only Way to Fight Inflation

25:16 Repricing of Risk Is Possible

30:56 The Sovereign Bank Doom Loop

38:47 Gold Is Now the Second Most Liquid Asset

41:19 Recap

43:32 Outro

TRANSCRIPT FROM VIDEO:

Historically gold is the last asset standing. That’s what you need to have in your portfolio to protect the wealth that you’ve accumulated to position you, to take advantage of this big crisis, because this next piece is not gonna be just a recession. I promise you, but there’s only one way to fight recession, which is deflation and that’s with inflation. And they got nothing to lose because they’re at the end.

The IMF just came out with their 2022 Global Financial Stability Report. And guess what we found out, coming up.

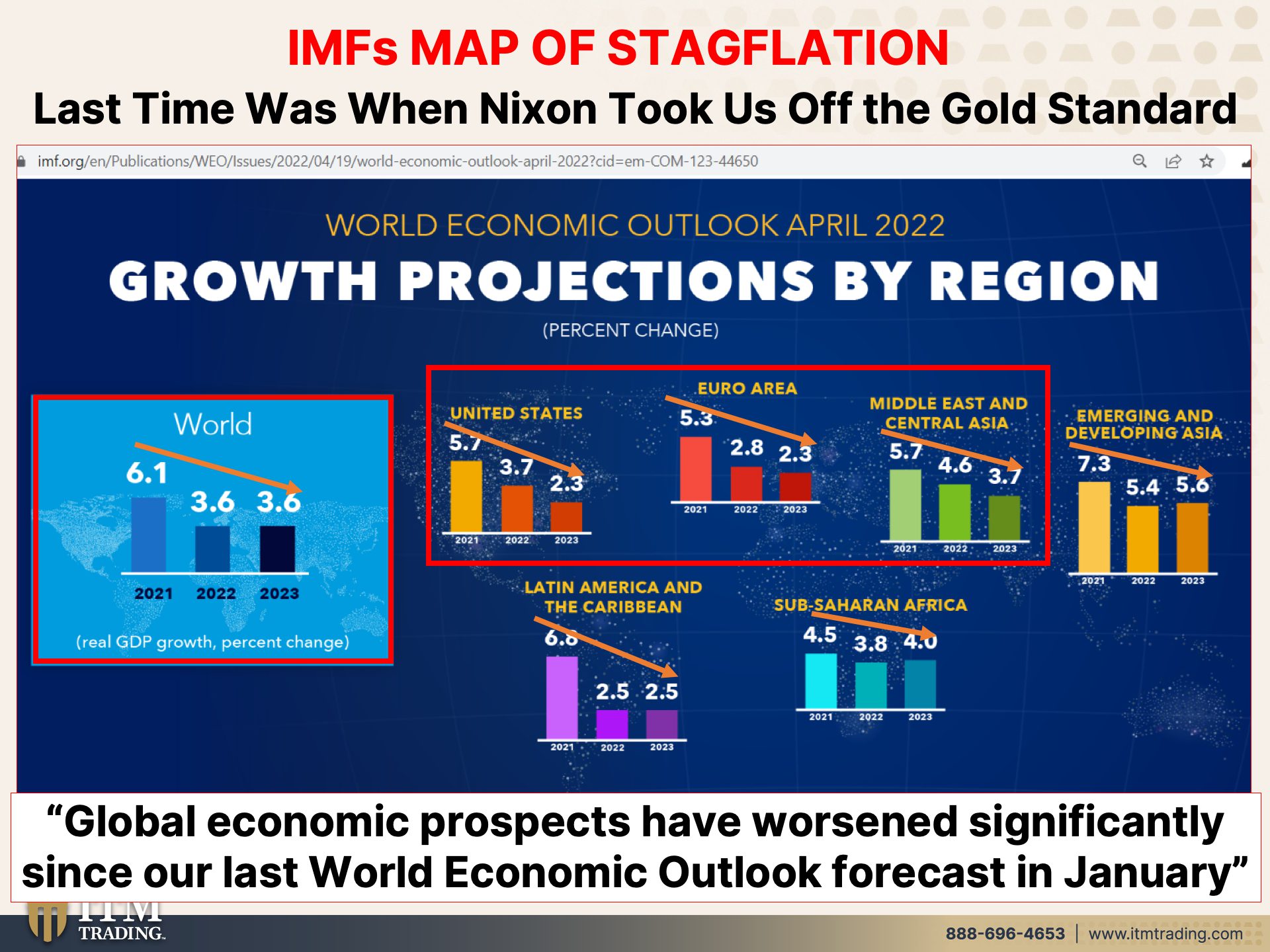

I’m Lynette Zang, Chief Market Analyst here at ITM Trading, a full service, physical gold and silver dealer, specializing in custom strategies. Cause everybody’s a little different, but you know, the IMFs really gave us a map of stagflation. Now I’m going to refer back to this a number of times, but I’d like you to remember. I lived through it. If you’re, if you’re my age or older or even a little younger, you’re gonna remember this, but we also were dealing with stagflation in the 70s and quite there are more parallels, so let’s move forward.

Here’s their map, okay. Wow. Look at this global growth projections go down. Now I wanna point something out because the world in 2022 is expected to shrink globally to 3.6% in growth, but then it’s gonna stay level. Why do you think that would stay level when you have the U.S., The Euro area and the middle east and central Asia all declining, really markedly even into 2023, not a big shocker. Oh, well maybe it’s because they anticipate that in Latin America, in Sub-Saharan Africa and in Latin America, the Caribbean that it’ll either stay the same in 2023 or get a little bit better. Is that so they could show the world stabilizing in growth in the next year in 2023? I don’t think this is really gonna look <laugh>. I don’t think this is gonna turn out the way this map shows. I think it’s gonna be much, much worse, but what they say is global economic prospects have worsened significantly since our last World Economic outlook forecast in January.

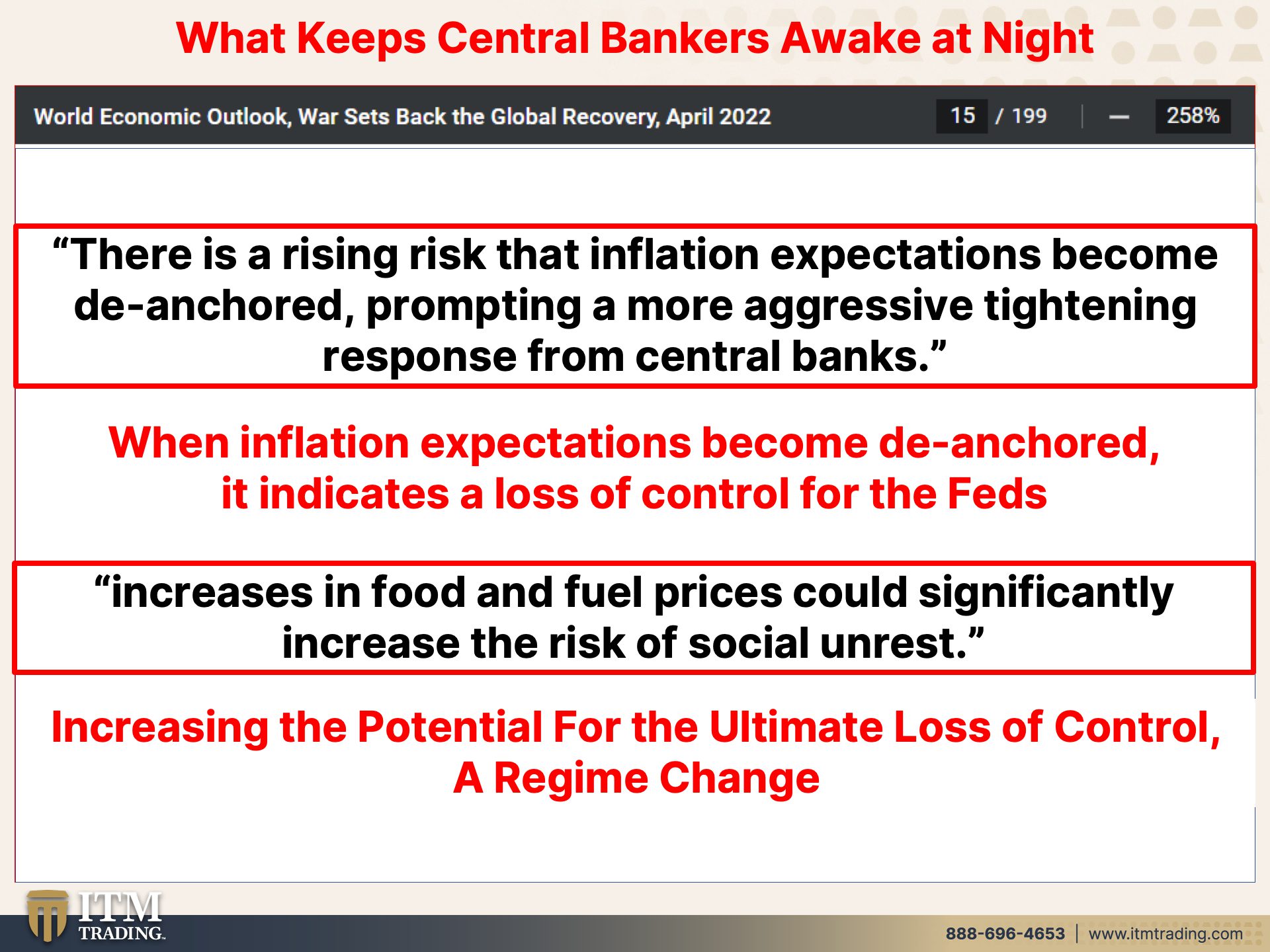

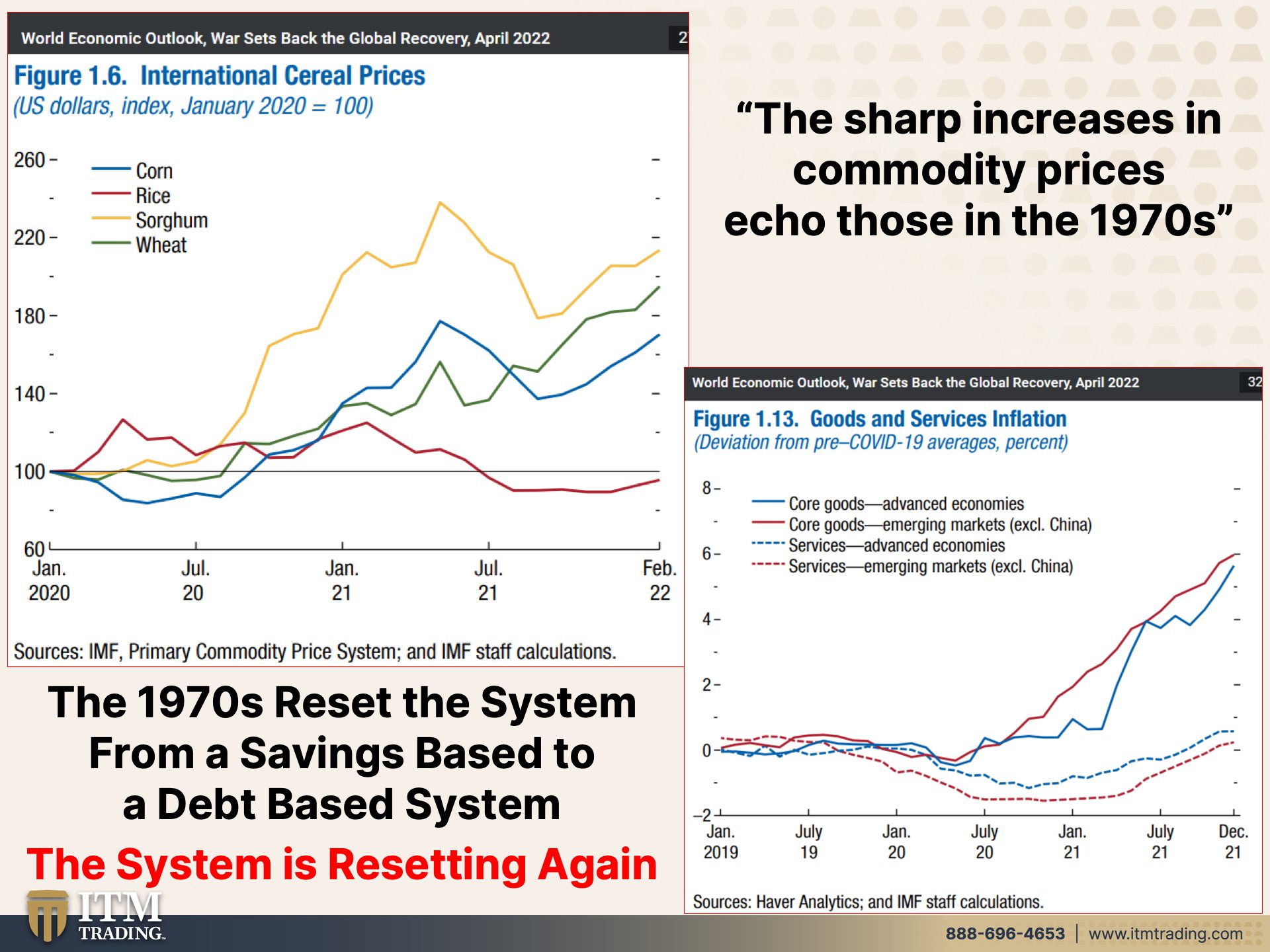

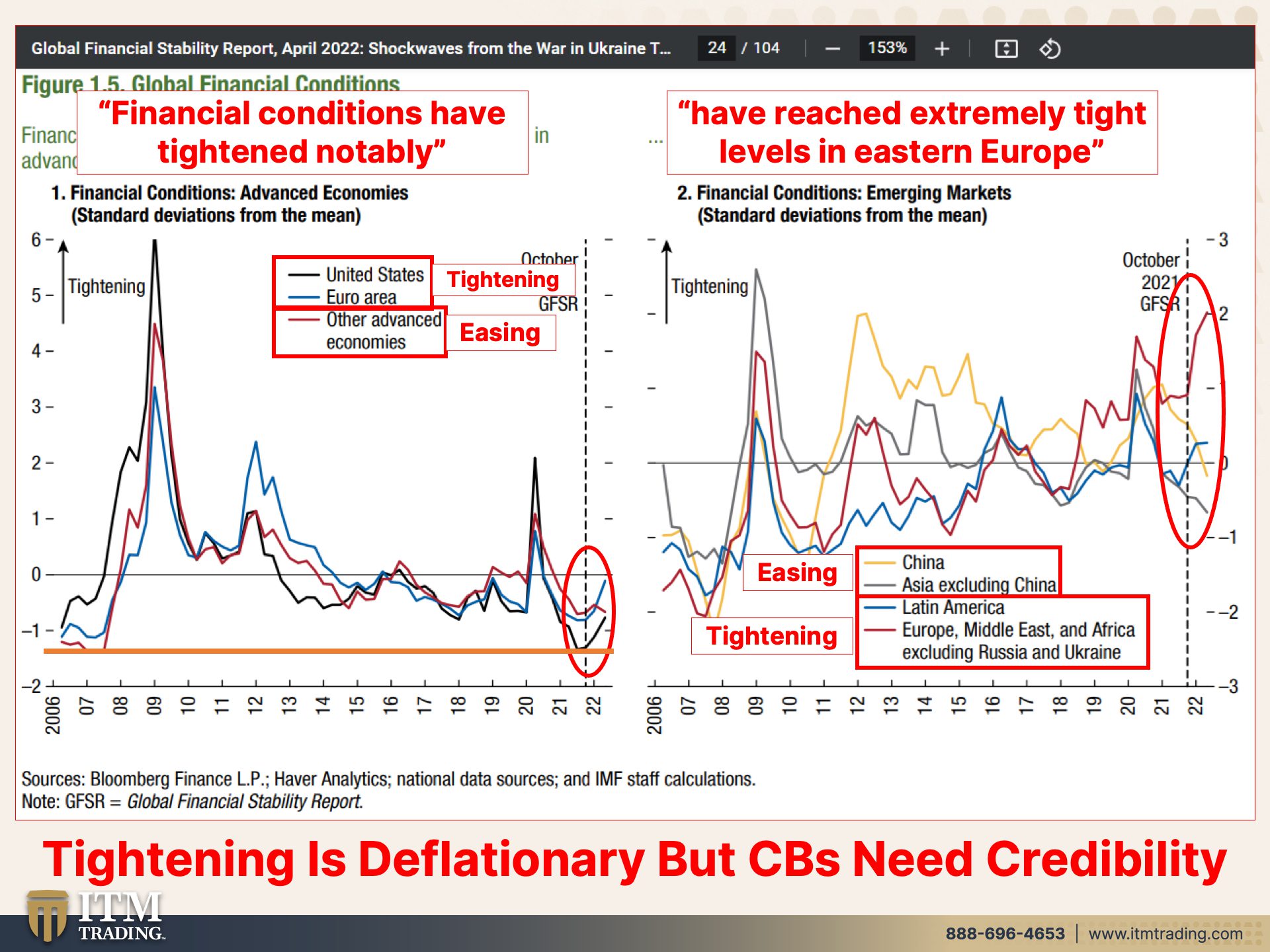

Yeah. Well, doesn’t take rocket science to see that, but let me show you what keep the central bankers up at night because they’re totally up. In many countries, there is a rising risk that inflation expectations become de-anchored a more aggressive tightening response from central banks. So what they’re really saying here is that the expectations indicates a loss of control because it’s a loss of confidence. If they don’t think that the Federal Reserve or any Central Bank, if the, if the public does not think that they can control this inflation, then that is a massive loss of confidence. This is a con game. It requires confidence. So this totally keeps the fed and other central banks up at night. Additionally, it increases in food and fuel prices could significantly increase the risk of social unrest. And so what they’re really saying in here is when people are hungry and hopeless, they make choices they would not otherwise make. They lose the confidence. And then this increases the potential for ultimate loss of control, which is a complete regime change. Now, mind you, the powers that be have a regime change in mind for us, socially, economically, and financially, but they wanna stay in control of the shift. And so they wanna stay in power on the other side of the shift, this could very well be the opportunity to make some positive changes for the people, because I don’t really want the people that got us into this mess to begin with, to remain and good control and empower. You think it’s gonna be different on the other side? Yeah, I don’t think so, but we are on the precipice. If, if it’s already started actually of a global food insecurity issue and I’ve been telling you for so many, that food is the single biggest issue for people as we go through these transitions, Food, Water, Energy, Security, Barterability, Wealth Preservation, Community and Shelter, get it done. If you haven’t moved forward on these issues in a very powerful way, then I’m sorry, but you are behind the eight ball. So we need to just move forward powerfully and get it done because the sharp increases and commodity prices echo those of the seventies because we changed. We had a regime shift change from a quasi gold standard anyway, to a pure debt based standard where we handed over complete control to these central bankers. So between the government and the central bank, there’s no purchasing power left and we’re going into a hyperinflationary spiral because they have to burn off all the debt that they’ve created. And here you go. I mean, I’ve been saying for a while that I think that this is the start of it, time will tell, but I’m, I’m pretty sure I’m right. I mean, I hope I’m wrong, but I, I, I don’t think so. I don’t think so. And frankly, I ordered more food from Azure Farms this morning, but we’re also seeing a spillover. So this is what they’ve been talking about quite a bit, because it’s not just contained in the areas that they like to take out of the of the inflation numbers, food and energy. So it is spilling over into goods and services as well. And we’re looking at slowing growth and rising prices that stagflation. The 1970s reset the system from a savings based system into a debt based system. And I have to tell you, we need to be back on this savings based system and the government is not going to do that for you. You have to become your own central banker and do it for self. This is your protection. This has been proven to protect you from inflation and the ravages of it for thousands of years over and over and over again. And you’ll see what I mean a little bit further along because we know the system is resetting again it had to, it died in 2008. It’s just been on life support and all that life support means that all of the systems inside the body of the global economy have shut down. They are addicted to this free money and now they have to take it away. And so what we see are global conditions tightening. In other words, interest rates are going up. The central banks are not buying as much of the government’s bonds and debt. And as well as going into the open market to buy corporate debt, like we saw them do not that long ago, etcetera. And there’s something that’s really interesting in here. Okay. Anything above this line, anything above this line is considered tightening anything below that line is considered easing, right? So making monetary policy easier right now, interest rates at zero, and the ability to borrow as much as you want for most corporations have certainly enabled the stock market, the real estate, all of the increases that we’ve seen in this inflation, because between 2008 and 2022, there has been a massive amount of liquidity, new money pushed into the market and also lots more debt. And I want you to keep this in mind because the tightening also threatens liquidity, which we’re gonna talk more about in just a minute. But the other thing that I wanted to really point out to you is that it’s in the, the United States and in the EU are kind of tightening. I mean, they haven’t really done it yet, but just talking about it over and over again has actually created some level as you can see of tightening. It’ll be interesting to see what they actually do and not, not what they actually do, because we know they’re gonna raise rates and here in the U.S., They’re gonna raise ’em by 50 basis points. Cause that’s shock at all. Except everybody, the they’ve been telling about us for so long that markets traders have gotten into position. Have you gotten into position? Because the markets, the traders in the markets have totally gotten to position. But what I really wanted to point out is that the level of easy money is the same as it was here in the U.S. Back in 2007, before the system broke from so much easy money, it’s like, you know, I should have had a pitcher with, with water and let it spill over because you pour all this free money. You pour it, you pour it, you pour it at some point, it’s gonna spill over, shocker! Look, we printed all this money and we haven’t had inflation, oh garbage. They had inflation in the stock market and they had inflation in the bond market and they had inflation in the real estate market. and it’s really all about those big bets, derivative bets that are placed on top of those. That’s really what makes this so extraordinarily dangerous. And in some places they’ve reached extremely tight levels in Eastern Europe. Yeah. I don’t think we’ve seen the last of this. And also you can see that in China who is pledging to keep supporting the economy. I mean China’s the a yellow line. And can you see how that’s gone back into easing? Because I mean, it’s just a mess over there. They’ve shut down their economy again. And boy shocker! That that influence is spreading globally and making supply systems even tighter in not just commodities, but also in goods. And it’s killing their economy too.

You know, sometimes when I see this stuff, honestly, you never really know. I mean, we make assumptions that they want this to keep going, but just think about the fact that they know that this is the end, because they’re looking at all of the data and they see it.

Maybe just maybe a lot of these crisis that we say unfolding. And if you were alive in the sixties and seventies, like I was, it was crisis to crisis, to crisis, to crisis. There were lots and lots of crisis around. So you’re paying attention here. You’re paying attention there. You’re paying attention there. While what they’re really doing is shifting the ground underneath your feet, the financial system, the money system. And you don’t know it because you’re already off balance on everything else I can tell you. I can promise you in July of 1971, I had a $20 bill in my pocket. In September of 1971, I had a $20 bill in my pocket. Maybe it was even a brand new bill. I did not know! Nobody. Most nobody, central banks knew government knew, but the general public, no idea that anything had changed. And we were, you know, keep calm. You know, Nixon told us if you buy American products, you’re not gonna have to deal with inflation. It was garbage. It was absolute garbage. And it’s garbage now. These patterns repeat, and I can’t sit here and tell you definitively that all these crisis crisis to crisis, to crisis, to crisis, that we are lurching from crisis to crisis with. I can’t tell you that this is not part of the intent to keep everybody off balance so they can make the shift and remain in power. You don’t want them to remain in power. I’m telling you right now, do not want them to.

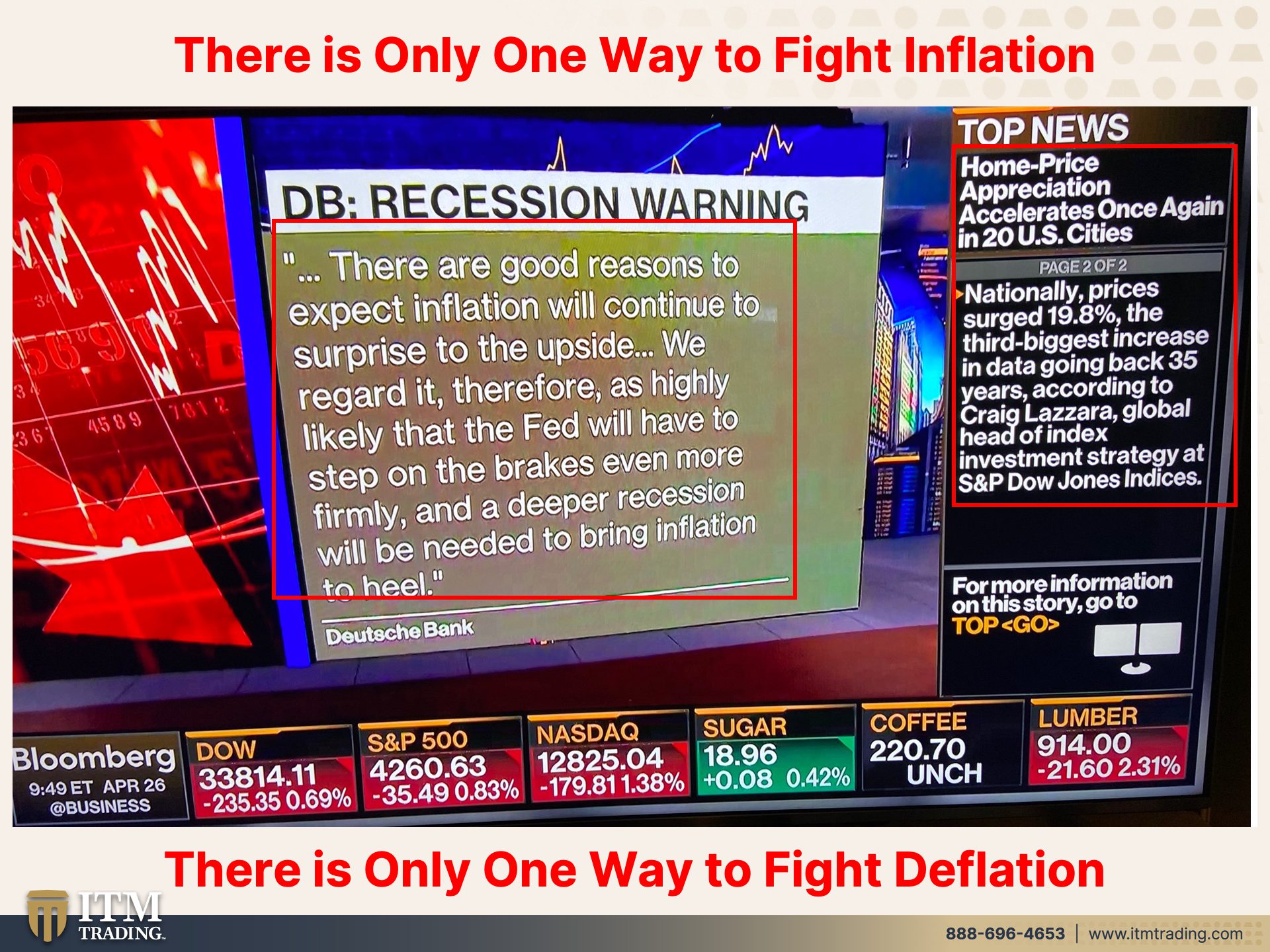

But China and Asia excluding China are easing, where Latin America, Europe, the middle east and Africa, excluding Russia and Ukraine are tightening. Yeah. But you see this tightening is deflationary, but they have to do it because it’s a con game. It requires confidence and they have to do it for their credibility. They have to. But the reality is, is there’s only one way to fight inflation and that’s with deflation. And there’s only one way to fight deflation. And that’s with inflation. They’re between a rock in a hard place. I don’t care what they decide. It’s all gonna be a problem.

And I thought this was so interesting that I caught. And this is from Deutche bank recession warning. There are good reasons to expect inflation will continue to surprise to the upside much as we hear it’s gonna moderate in the second half of this year. No, we regard it therefore as highly likely that the fed will have to step on the brakes even more firmly. In other words, raise rates more and to deeper recession will be needed to bring inflation to heal <affirmative>, but they can’t do it. They won’t do it. I’m gonna put my neck on the line here, and I’m gonna tell you, they’re gonna have to try. So I’m not saying they won’t raise rates, but they will change that as the economy, as the global economy, as the U.S. Economy completely craters. And it will crater, if they do 50, 50, 50, 50, because there’s so much debt that’s coming due and must be either paid off or rolled over or defaulted upon. Remember all the zombie corporations that we’ve talked about over the years, that’s just gotten worse. So it’s funny because somebody was kind of making fun and of it the other day and said, well, the zombie apocalypse, you know, it’s not these walking dead that are gonna come and eat your brains. It’s the walking dead corporation that will take down the whole system because it will trigger a level of derivative default, most likely, that they will not be able to cover up it’s those that create this mess that could, that can determine whether or not there’s a default. I mean, it really is. It really is. It is, is a very sad joke. But on the top of this or on the side, rather, I should say of the recession warning, what do we have? I mean, that would is just lucky, happenstance, frankly, home price appreciation accelerates once again, in 20 count 20 U.S. Cities, nationally prices surged 19.8%. The third biggest increase in data going back 35 years. Okie dokey then. So you got home prices going up 20% and you’ve got inflation. Yeah. It’s only at 8.5%. Do you believe that? Have you been to the grocery store? Have you been to the gas pump? Do you really think that these are temporary? Because frankly I don’t, I don’t. And how in the world can people afford to live? When people are hungry and hopeless, they make choices they would not otherwise make.

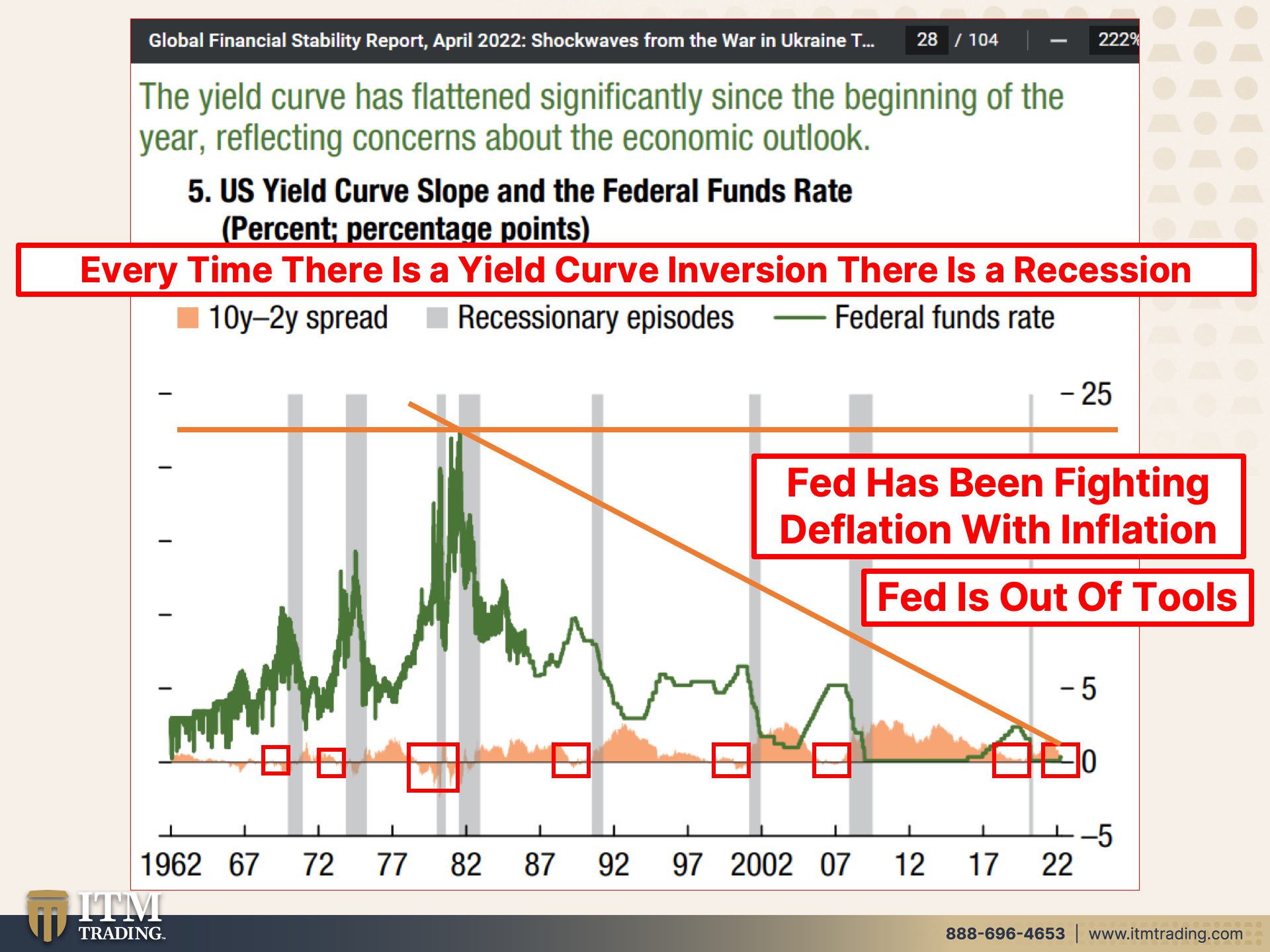

So I thought that this was also really important to show you. And there are a few things and there are some things in here I didn’t even mark off, but I definitely want to talk to you about, so they say the yield curve has flattened significantly since the beginning of the year, reflecting concerns about the economic outlook. And frankly, we had an aversion. The fact that they managed to manipulate that inversion away does not because they do it every time does not, not negate. The fact that we had a yield curve inversion, and frankly the five year is still inverted above the 10 year. Is it inverted against the 30 year? I’ll have to look. It might be because it typically is. So we have a yield curve inversion, and every single time there is a yield curve inversion. There is a recession. Here you go. Can you see it? right? Now, this is the Fed funds rate. And this graph goes back to 1962 and you can see what it looks like until we hit 1986-1987, when they have clearly gotten control. But look at the ramp room. They talk so much about Paul Volcker. First of all, and you can see intra day, the yield were actually 21.5% intraday. Can you see Fed chair Powell boom, raising rates to 21% not gonna happen! Because we’re at the end of the system. That was the beginning of the system. This is the end of the system, but look at how kind of choppy and thick these interest rates were. And now it’s all nice and smooth. Isn’t that interesting because what the fed has been fighting is deflation over all these years. And there’s only one way to fight deflation and make no mistake about it. A stock market going down a real estate market going down that is all deflationary. There’s only one way to fight it. And that with inflation. So look at it, they dropped their interest rates on average five and a half, five, and three quarters percent to stimulate that borrowing and spending to keep those assets inflated and the cheaper it is to borrow. Why do you think, what do you think one of the real reasons why we’ve seen this massive increase in house prices? Because they’re basically giving the debt away for free. Well, what happens if that changes? Now, I want you to think about this because wall street, after 2008, that was a setup for Wall Street to come in and make a big mark in the real estate market, which is exactly what they did buying up a tremendous amount of real estate. And then what do they do? They convert that, or turn it into a financial product that’s financialization, and then sell it back to you. You are the one in your pension and your IRAs and your 401ks, etcetera. You are the one that is going to eat it in the shorts. If you own these products, that’s why if you can’t take it out or do anything else with it, or even if you can and you choose not to, that’s your choice. I’m not telling you, you, you gotta do what your car comfortable with regardless of what I say, but you need to have a diversified portfolio to protect this. We have historic formulas that give us a good darn gauge on what, on how much gold you’re likely to need to protect that wealth. So we’ve got it all in formulas. You call us, you talk to us, we’ll tell you how much you need. That’s easy peasy, but they’ve been fighting deflation. And now they’re outta tools. Why are they outta tools? Cause we’ve been anchored at zero since 2008 over here. And the attempt to raise rates is really about having the ability to lower it again to inspire higher inflation. So you tell me what they can do. They’re trying to raise rates just so they can lower them again, but we’re going from crisis to crisis to crisis. So really, it doesn’t matter. But if you have variable rate debt, you better get it paid off as quickly as you can, because that puts you in massive jeopardy. This is really significant. This is a really significant graph. And what I’m trying to show you here. I mean, this is the IMF showing you, this is the federal reserve showing you. Can you see it? Because frankly we’re at the end, when? We’re at the end now! A challenging normalization process. You think? What in the world is normal about anything that’s been going on since 2008? Nothing except that they remain in control and they transfer your wealth, but they’re doing it a lot faster. Stop them. How do you stop them? This is how you, them, you take it out of the system in something that has full utility, always demand. You don’t want gold just cause it’s gold. You want gold because it protects you from inflation. It protects you from political unrest. It protects your wealth and you’re purchasing power. That’s why simple!

A repricing of risk is possible. Well, look at the markets, you think? That’s a repricing of risk because as long as you had free money and they could pump up those stock markets, for example, earnings were irrelevant. I mean, it wasn’t really all that long ago. Do you ever hear about unicorns anymore by the way? No, but you heard about ’em all the time when they didn’t have earnings, they weren’t gonna have earnings as far as the, I could see and they were worth billions and billions of dollars. Well, with interest rates rising, that changes that equation. It really is just that simple and much as they want you to believe that all of this money print, sorry, Edgar. Oh, we have to fix this. All of this money printing did not have any impact on inflation. Oh, oh, those were all contained garbage, garbage, garbage. And now that they’re being forced to take that free money punch bowl away. There’s an awful lot of thirsty traders out there. I hope you are not one of them. They say that all that did all the QE did was a 50, 60 basis point compression in interest rates yields? Garbage. It’s much higher than that. All the Medling much, much higher, but not for you or me, it’s for the corporations because they’re far more important than we are. And at this point they’re are no good options. They keep the free money. Well punch bowl rolling. Then that will just exacerbate the, the inflation that we’re dealing with. They take the punch bowl away. That creates a deflationary environment because stock markets are being volatile and going down and real estate markets. Well, those are still going up, but you gotta have a place to live. You don’t have to own a stock, but you gotta have a place to live. You gotta have that Shelter, Food, Water, Energy, Security, Barterability, Wealth Preservation, Community, and Shelter. Get it done, get it done. You’re not gonna know the day before. And even if you did know the day before, you would not have time to get everything in place.

I can’t even begin to tell you how thankful and grateful I am. That the universe put me in this space to understand what was happening. I started prepping well, I started with the gold and the silver, because if you don’t your wealth first, it’s kind of hard to do anything else. But I bought this property and started an urban farm. I’m not a gardener. I’m not a farmer. I am an urban farmer now, but I certainly wasn’t when I started this because I a hundred percent knew Food becomes the single biggest issue for people. We, we don’t know how long this is gonna last, but what we do know is it’s here, it’s here.

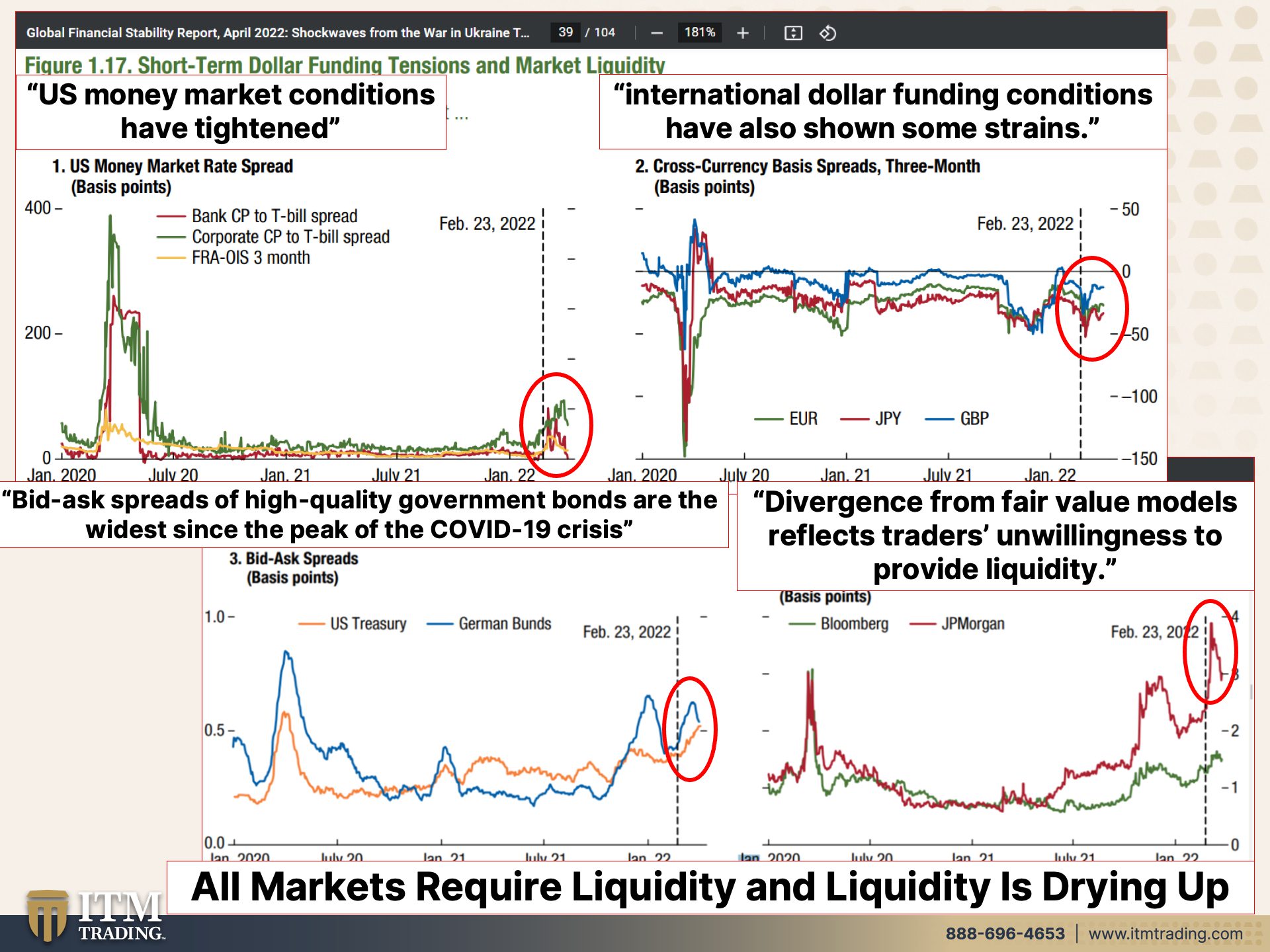

So short term, dollar funding, tensions and market liquidity market liquidity is your ability to buy and sell easily without dislocating prices, that’s market liquidity. So the more money flowing into an area, the more liquid that asset or that instrument is. So with all that free money, made the markets really, really liquid. But now that is starting to change. International dollar funding conditions have all also shown some strains because how many times have we talked about the corporations that have issued debt in terms of dollars? They don’t own dollars, but when they have to make an interest payment or a bond payment, they have to pay in dollars. So this is really just in theory. You’re gonna see this whole thing fall apart. I promise you, you will. But when the fed raises interest rates, or even when interest rates on government debt goes higher, well then that’s supposed to have an impact on gold because after all gold, doesn’t pay you an interest payment. Well, I’ll tell you what a trillion times zero is zero, and I’ve shown you ad nausea, probably how low the purchasing power has gone. There’s no purchasing power left. The only thing keeping the dollar viable is your confidence. And that confidence is going away too. The bid ask spreads of high quality government bonds are the widest since the COVID 19 crisis high quality because they can print the money that they need to pay you. Oh, that makes it high quality. All right, well look, I got a bridge in Brooklyn. You interested? I can sell you that bridge in Brooklyn. Don’t buy it. Absolutely don’t buy it.

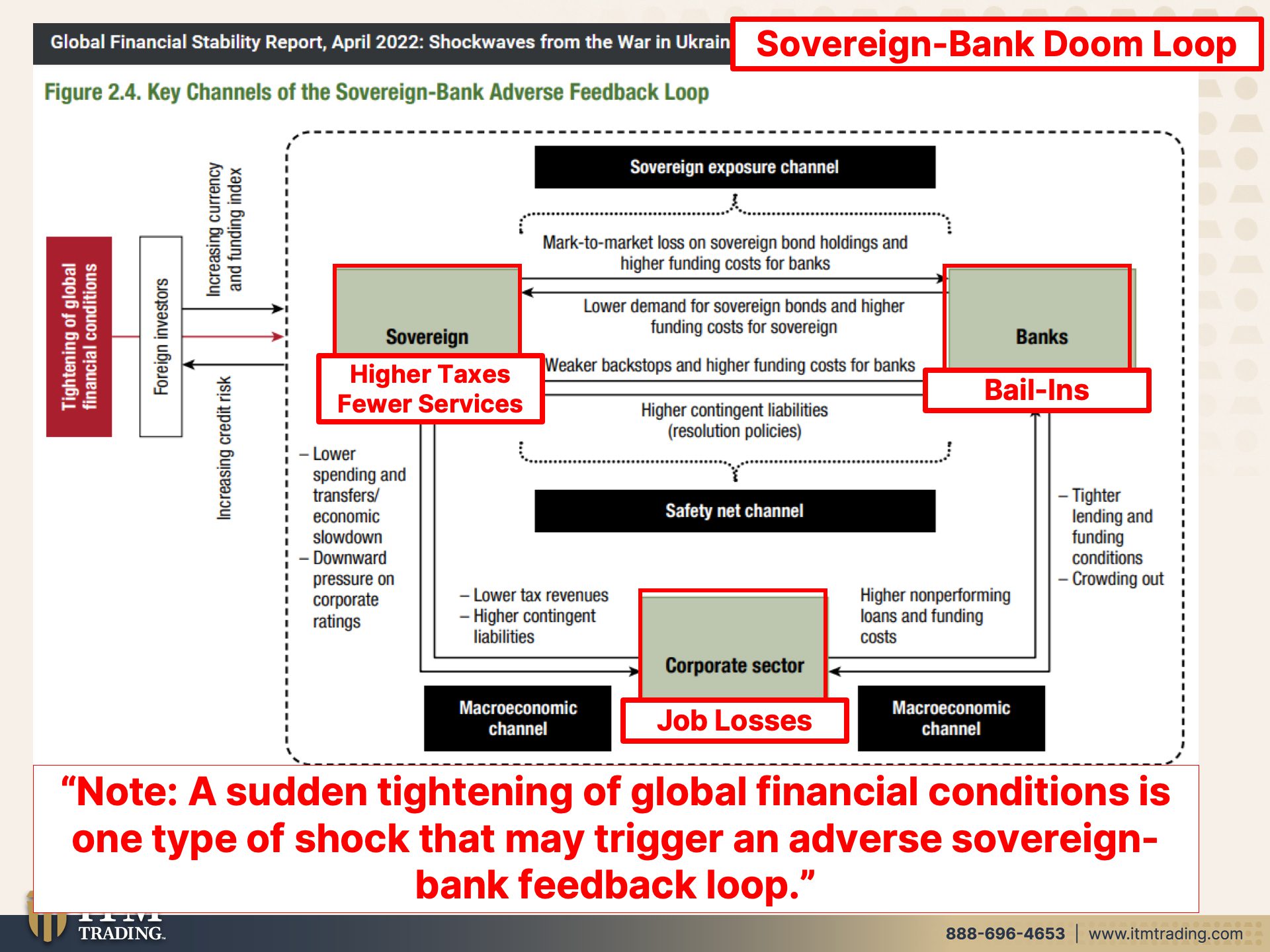

Because the reality is, the liquidity is drying up and here’s how it impacts you. This is the sovereign bank. You kind of remember, we were talking about this back in what, 2013-20`14 with the sovereign debt crisis with Greece and, and Europe. I mean, it was was all over the place and there, and it created a doom loop between governments, which are sovereigns and banks. So here the IMF gave, gave us this beautiful little flow chart on how that is, but without going into that in too much detail, this is really what you need to see. And the note is a sudden tightening. So central banks, raising rates substantially a sudden tightening of global financial conditions is one type of shock that may trigger an adverse sovereign bank feedback loop. This is called a doom loop, but they didn’t wanna say that in here, but that’s what it’s called. Because with the government debt, you have to have confidence in your government or you topple the government, you topple that power. They don’t want that. They don’t want, they wanna remain in power, but when government bonds aren’t you know, easily purchased around the world, well, and governments need money to continue to run the government and the army. They raise taxes and they reduce services. We actually saw that quite a bit in Chicago several years ago when they were having their own government debt crisis. So higher taxes, fewer services and job losses, because this transmits to the corporations, all right, we’ve got a very tight labor market. Of course they want a two-tier labor market. Kind of like China did a report on this. I don’t know, several, several, several months ago with the lay down economy where, and we’re seeing it here too, in this very tight labor market where people are reassessing, what the value of their time and work is. So right now we have a tight labor market, but we go into a massive recession. You’re gonna see job losses. And then that translates into the banks bail in anyone? You better not have too much cash sitting in the bank that you can’t afford to lose. So that too needs to be protected. Even if you have to, like, I have to keep a certain level of cash because I’m running a business and I have salaries to pay and all that kind of stuff. Right? But I offset, if that all goes away, if they bail that in and yes, you’ll say FDIC insurance. There’s not enough money in there to if too many big banks or too many banks go out at once. We saw that in 2008, they were one bank failure away from it being obvious. So if that does, it’s not a big deal to me because I’ll just convert some of my gold into whatever cash I need to keep my business running. So that’s security, that’s savings, that’s protection. So you really need to think about it because they’ve been testing this. They know how this works and what are you gonna do? You’re gonna go bang on the doors, give me my money. It’s not your money. You loan it to the bank. I just got 15 cents an interest on my business, checking account, 15 flipping cents. <Laugh> you know why I got 15 cents? Because my guys, I got 15 cents, cause I’ve loaned them that money that I’ve deposited in there. Yeah. Yeah.

So here’s the kicker, rising liquidity and funding risks. I’m gonna read you this whole thing. There are some signs that the sharp rise in market volatility, severe disruptions in commodity markets, the LME, and the perception of rising counterparty risk may be starting to weigh on dealer bank’s balance sheet capacity and appetite for intermediation, meaning they’re not sure they’re gonna get the money back so they don’t wanna lend it out. Remember, we saw the same thing in 2008, with that interbank funding, boom, dropped like a stone without with implications for liquidity and funding conditions as well as broader market funding, they are scared to death that the banks won’t do the job that they need them to do, which is provide liquidity, buying and selling these assets so that they create a market. But that’s been changing for a while. I’ve done videos on that as well. By the way, just wanna point this out. Let’s see, where is it? Blah, blah, blah, blah, blah. Maybe starting to wait. Okay. Rising. Okay. So right here, the perception of rising counterparty risk, let’s see what financial here’s a test. You’ve heard me say it a bunch of times. What financial asset is the only asset. According to the Bank for International Settlements, that runs zero counterparty risk. I’ll give you a hint. You hold it, you own it outright. It runs no counterpart risk. You gotta hold it cause if you don’t, you don’t own it. Tensions in short term dollar funding markets have been limited so far, but strains are beginning to emerge, reportedly reflecting both precautionary motives to bolster liquidity positions. So in other words, starting to hold back some money if they run into trouble, but you know who funds those money that liquidity, the short term, liquidity? Money markets. Do you own any money markets? Or do you perceive that you own the money that’s in those money markets? No, no, no. Let’s see, reportedly reflecting both precautionary motives to bolster liquidity positions as well as growing concerns about credit risk. No counterparty risk spreads in short term, dollar funding markets have widened. In other words, the cost to borrow has gone up. This is a problem. Can you see this next crisis brewing? Are you ready for it? Are you ready for it? Cause this is gonna get you ready for it. As well as Food, Water, Energy, Security, Community, and Shelter. Get it done. Get it done. If I sound urgent it’s cause I feel urgent and I hope you feel urgent too.

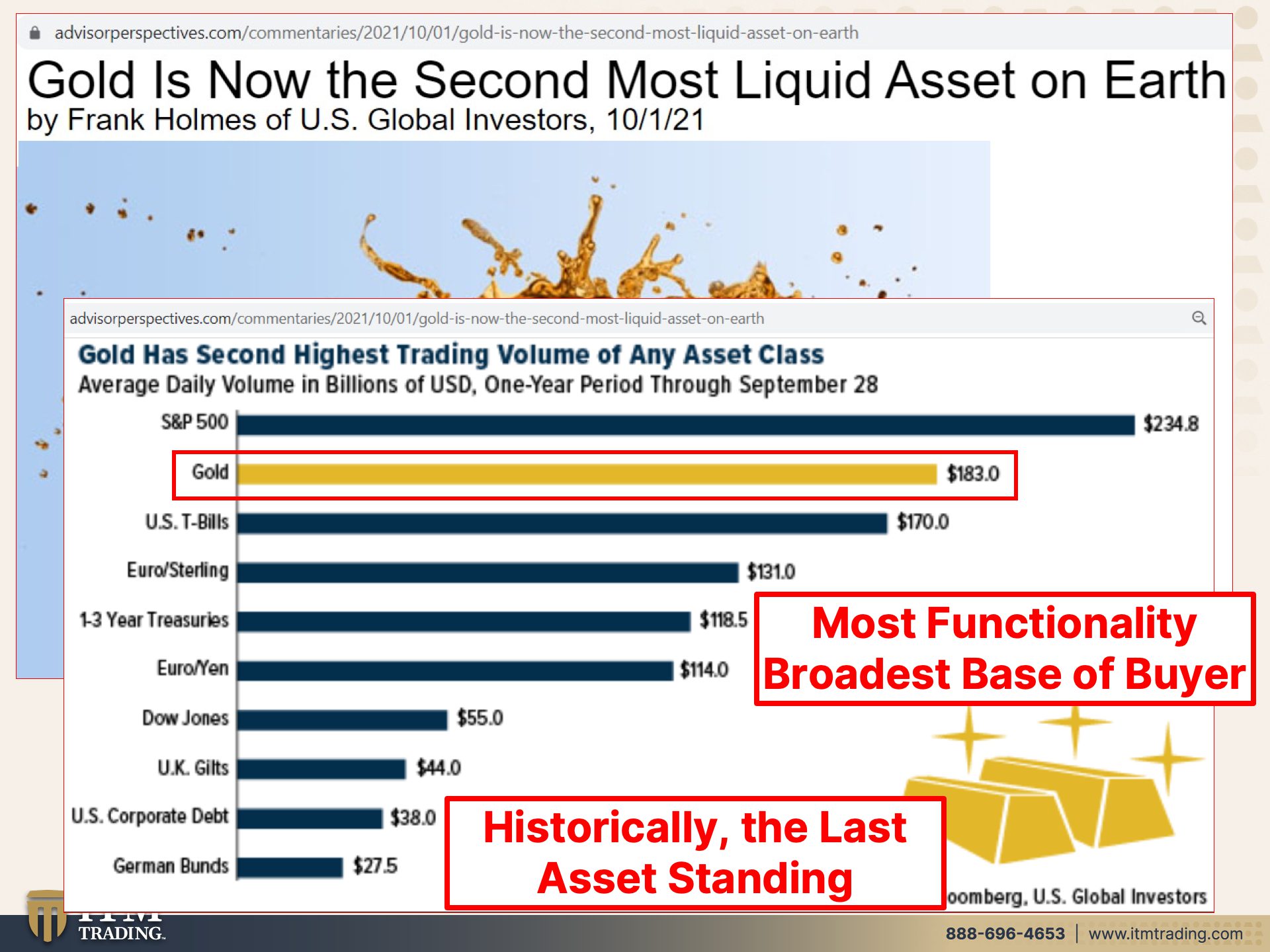

And shocker! Gold is now the second most liquid asset on earth. Guess what? Gold is about to be the first most liquid asset on earth. Look, it has the second highest trading volume of any asset class. And there is a rush to safety. This is proven thousands of years. It has the most functionality because it is used across the entire spectrum of the global economy, every single area, Financial, art, food, technology, medical, on and on and on every single sector. You tell me what else can say that what other financial asset? And it runs no counterpart risk. Historically gold is the last asset standing. That’s what you need to have in your portfolio to protect the wealth that you’ve accumulated and or to position you to take advantage of this big crisis because this next piece is not gonna be just a recession. I promise you. And I don’t like to promise this, but there’s only one way to fight recession, which is deflation and that’s with inflation and they got nothing to lose because they’re at the end. If you aren’t prepared for hyperinflation yet, get, get prepared. Please do yourself a favor. Do your family a favor. I don’t care what anybody else thinks. I’m showing you what’s happening. They’re telling us what’s happening. It’s just that most people don’t listen cause they’re busy living their lives. And I get it. I mean, I totally get it, But I wanna make sure that my family and it’s a broader family. It’s not just my children and my siblings. It’s it’s my ITM family here. It’s my, I don’t really ever say this word, but metalmamas family here. I wanna make sure that we all can survive this and even thrive through this. That’s the opportunity. It’s not all doom and gloom, but if you don’t get prepared.

But with all this doom and gloom, I gotta have a little bit of fun. And also there are some things that I’m dying to talk about that I don’t get to talk about on air. And I will on Saturday, June 11th at the Grand Wailea on Maui. That’s a Saturday. So I hope you can join us. The link is below, right? Mm-Hmm <affirmative> the link is below and it’s a very, very small intimate group. I think we’re almost done. Yeah, we’re we’re almost done. I think we just have a few spots left. So make sure that you watch my interview with Security expert, Bill Blickensderfer on the Beyond Gold and Silver channel and that’s out now and also on the ITM podcast, leave us a review on Apple or Spotify. Listen to us anywhere, anytime on all major platforms, we’re here for you and if you haven’t already, or even if you have, but you haven’t finished it off, you need to really click that Calendly link below. Talk to our consultants to set up your own per strategy and have some goals in mind. And if you don’t quite know how to do that, we’ll help you. We have questions that we’ll be able to ask you. That’ll help you determine what are your priorities? What are your goals? And then we can put together a plan to help you support that. But your goals have to come first. So if you look like this, please give us a thumbs up. Make sure you leave a comment. It helps us spread the word even more. And this is a very important video share, share, share, have a pizza party and share it or something because maybe you can entice people to watch it. If you offer them some free food, it’s worth it so that you have some help in protecting those that you care about. And until next we speak, please be careful out there. Bye bye.

Join Lynette Zang in Hawaii: https://info.itmtrading.com/the-grand-wailea-maui-2022/