BANKS (3) / PUBLIC (0): Will You Agree?

Constitutionally the government is supposed to exist for the benefit of the public. We’re told that the Federal Reserve was created by congress to provide a safer, more flexible and stable monetary and financial system. It seems the way governments and central bankers interpret these roles is to make sure that, at all costs, banks remain profitable.

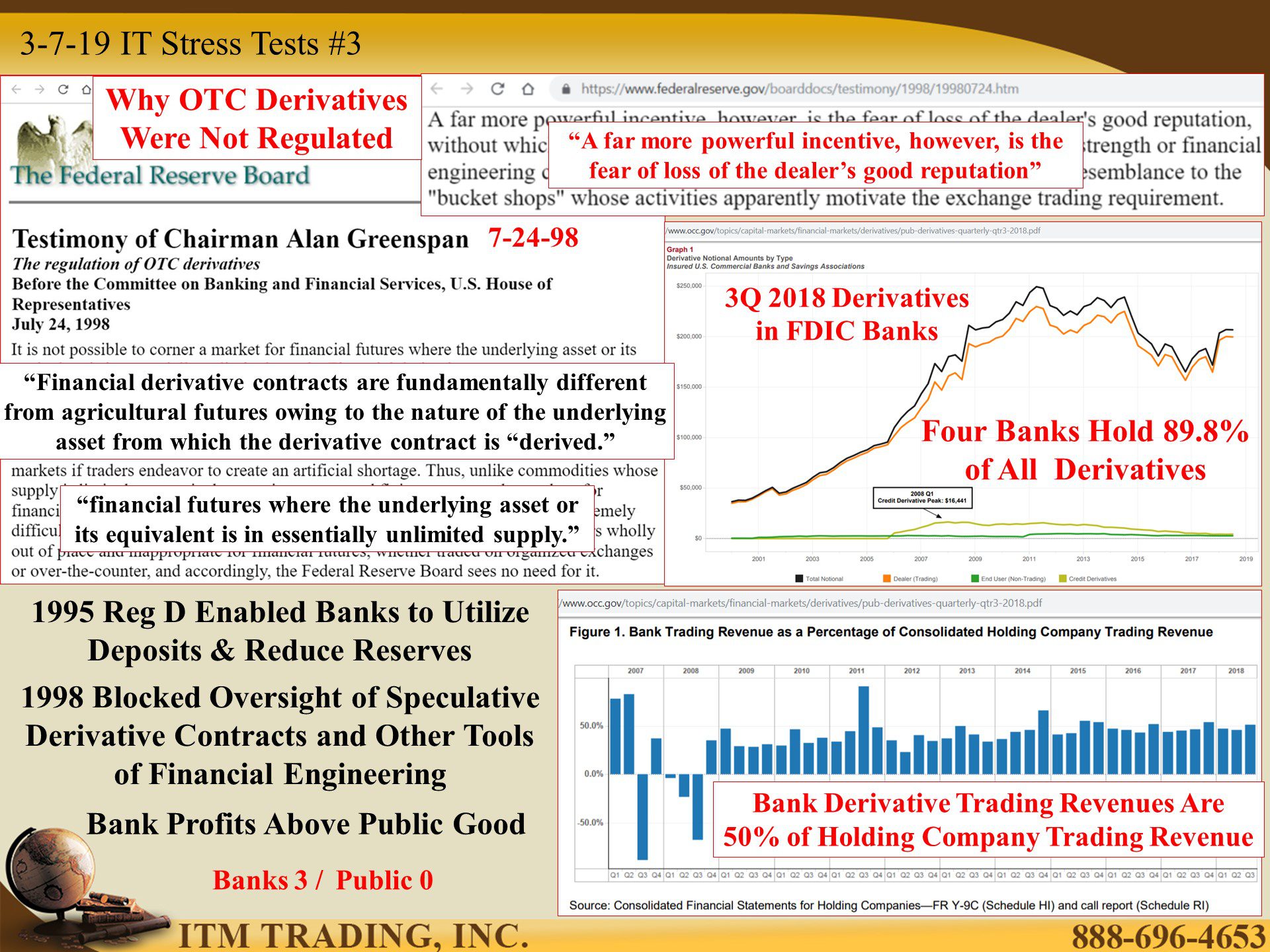

Today we’re looking at as three areas that, while making the banks richer, puts the taxpaying public on the hook for loses during the coming financial crisis.

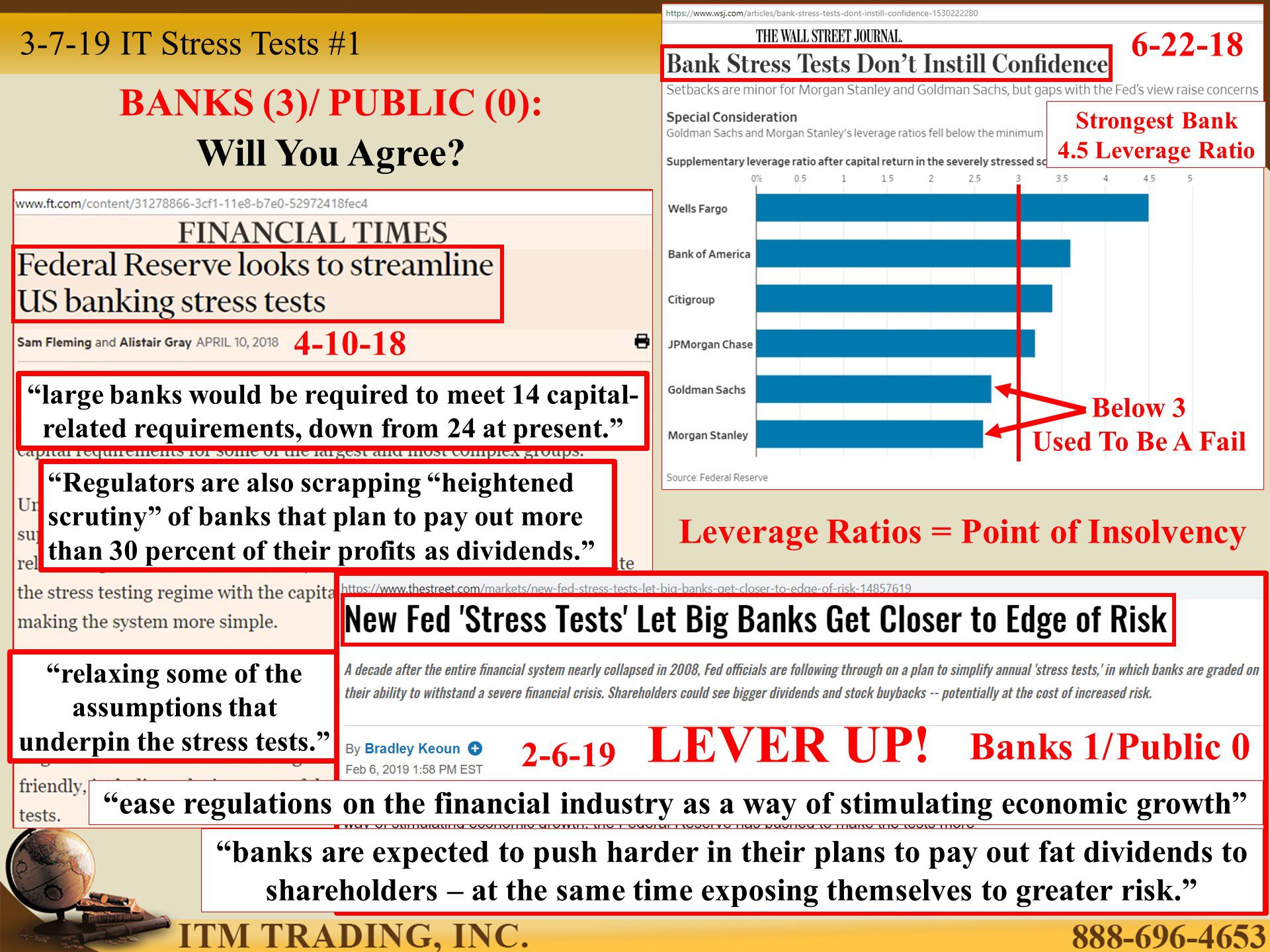

After the crisis that became apparent to all in 2008, bank “Stress Tests†were put in place to regain public trust. In 2018, every bank passed…with a little help from the Fed and regardless of their leverage ratio, which indicates how far their assets could fall before the bank would be insolvent (which does not necessarily mean they go out of business), every bank was able to payout to shareholders, at least the same amount they paid out the previous year. Doesn’t seem too stressful to me, but no matter, under the guise of streamlining the stress tests, large banks are now only required to meet 14 capital-related requirements, down from 24.

In addition, regulators are scrapping “heightened scrutiny†of banks that plan to pay out more than 30% of their profits as dividends and are also “relaxing†some of the assumptions that underpin the stress tests.

The reason? To “Stimulate†economic growthâ€. For who? The expectation is that banks will payout even more to shareholders as they take on more leverage and risk.

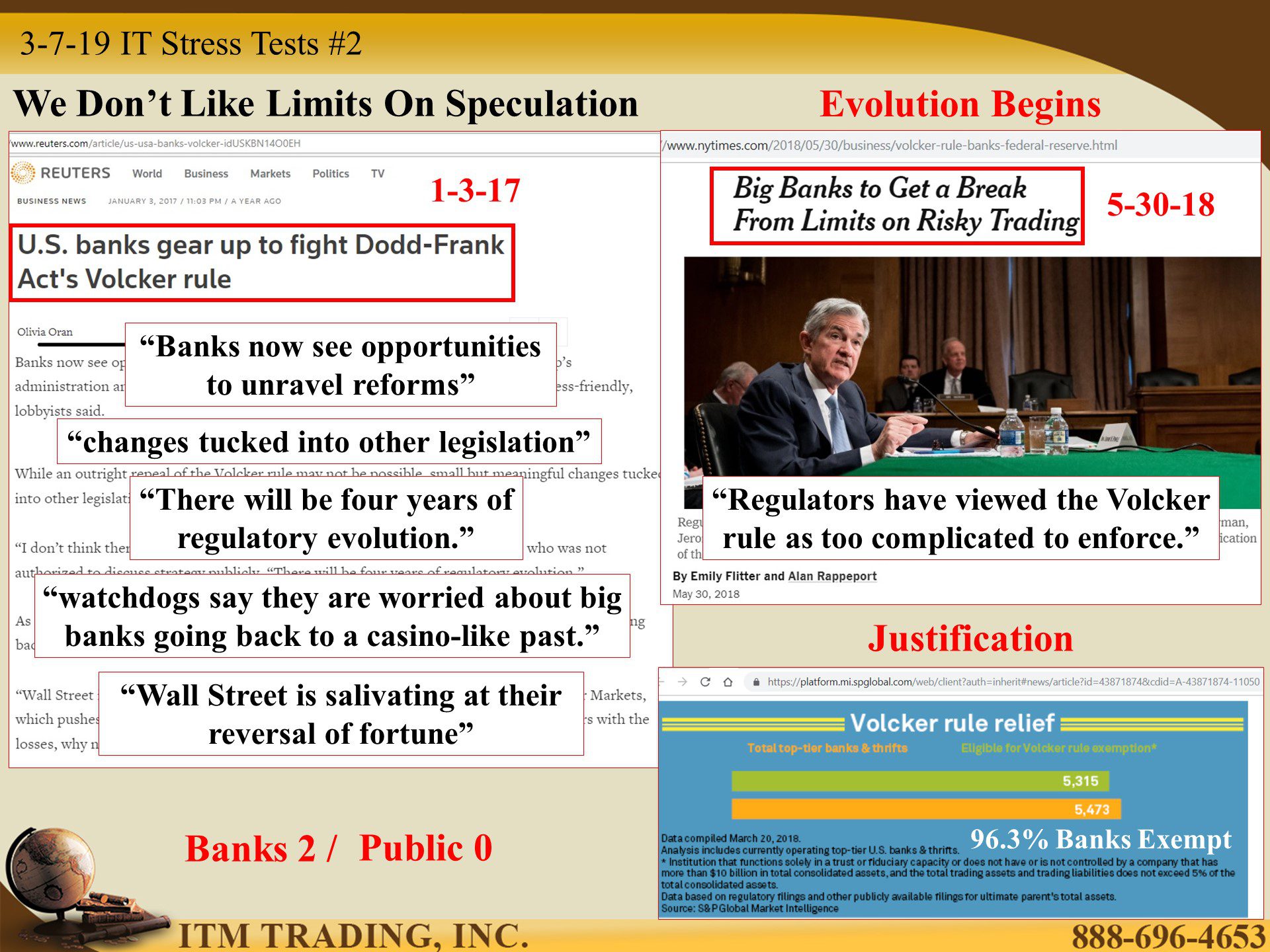

At the same time, the Volcker rule that limited speculative trading, is being nullified because central bankers have viewed it as being too complicated. They simplified it so much, that now, 96.3% of all banks are exempt. That should “Stimulate†growth in speculative trading, and perhaps, bank profits, which can then be paid out to shareholders.

Keep in mind that once this money is paid out, it is no longer available to be used during a financial crisis…but deposits are. Hello, bail-in.

Of course, these are just a couple recent legal changes that put your wealth in jeopardy, in a long line of changes over time. What can prevent your wealth from being bailed in? Have it out of the system in physical gold because, “gold and economic freedom are inseparable.†Alan Greenspan, Fed Chair 1987 – 2006.

https://www.wsj.com/articles/bank-stress-tests-dont-instill-confidence-1530222280

https://www.federalreserve.gov/newsevents/pressreleases/files/bcreg20181031a3.pdf

https://www.nytimes.com/2018/05/30/business/volcker-rule-banks-federal-reserve.html

https://www.reuters.com/article/us-usa-banks-Volcker-idUSKBN14O0EH

4.

YOUTUBE

Today we’re looking at as three areas that, while making the banks richer, puts the taxpaying public on the hook for loses during the coming financial crisis.

After the crisis that became apparent to all in 2008, bank “Stress Tests†were put in place to regain public trust. In 2018, every bank passed…with a little help from the Fed. In addition, regulators are scrapping “heightened scrutiny†of banks that plan to pay out more than 30% of their profits as dividends and are also “relaxing†some of the assumptions that underpin the stress tests.

At the same time, the Volcker rule that limited speculative trading, is being nullified because central bankers have viewed it as being too complicated.

What can prevent your wealth from being bailed in? Have it out of the system in physical gold because, “gold and economic freedom are inseparable.†Alan Greenspan, Fed Chair 1987 – 2006.